Reading depth

- 1. Industry — Why It Is Needed, and How Big It GetsDemand heads to 4x while capacity grows only ~10% a year. This gap is the root driver of the pricing cycle.Jump to section

- 2. Demand — The Simultaneous Supercycle AI Servers MadeDemand, lead times and prices all point up. The key question of this note is which stage the benefit flows to.Jump to section

- 3. Supply — Why It Does Not LoosenThe MLCC and FC-BGA shortage is a high-spec shortage, not a volume one. Physics, certification, and yield barriers make it a structural bottleneck.Jump to section

- 4. MLCC Finished Goods — The Stage Where Korea Really Is No. 2In MLCC finished goods, Samsung Electro-Mechanics is global No. 2 at ~40% AI use, the epicenter where benefit lands in Korea. The problem is upstream.Jump to section

- 5. Hidden Upstream ① Dielectric Powder — The Real No. 1 Is Japan's SakaiThe real No. 1 in dielectric-powder merchant supply is neither Korea nor China but Japan's Sakai. Murata self-supplies even its powder.Jump to section

- 6. The Full Vertical Value Chain — Leader and Nationality by StageMLCC and FC-BGA form a six-stage chain from powder to substrate, and Korea ranks near the top only at the two finished-goods stages. Japan holds the upstream.Jump to section

- 7. Hidden Upstream ② Nickel Powder and Release Film — Another BottleneckNickel powder and release film are also Japan- and China-held upstream. Samsung sources nickel via a Boqian LTA; the real structure is external lock-in, not in-housing.Jump to section

- 8. FC-BGA — Ibiden vs Samsung Electro-Mechanics, ABF Is AjinomotoFC-BGA pits Ibiden's defense against Samsung's pursuit. Samsung gains on diversification, sellout, and imminent NVIDIA entry, but Ajinomoto monopolizes ~95% of ABF.Jump to section

- 9. The Benefit Structure at the Finished-Goods Stage — How Price Leverage Falls Through to ProfitIn a shortage, a price hike by the global No. 2 falls through almost entirely to profit. A 10% MLCC hike adds about 600 billion won to Samsung's operating profit.Jump to section

- 10. Conclusion — Where Benefit Flows, Stage by StageThe key is structure, not one stock. Finished-goods benefit flows to Samsung, materials benefit to Japanese and Chinese makers. Read the chain as two layers.Jump to section

1. Industry — Why It Is Needed, and How Big It Gets

Before looking at who makes these parts and why supply stays tight, we should establish what they do and why demand is exploding. and hide behind GPUs and memory. Yet without them the AI accelerator does not run at all.

Why they are needed — power stabilization and chip connection

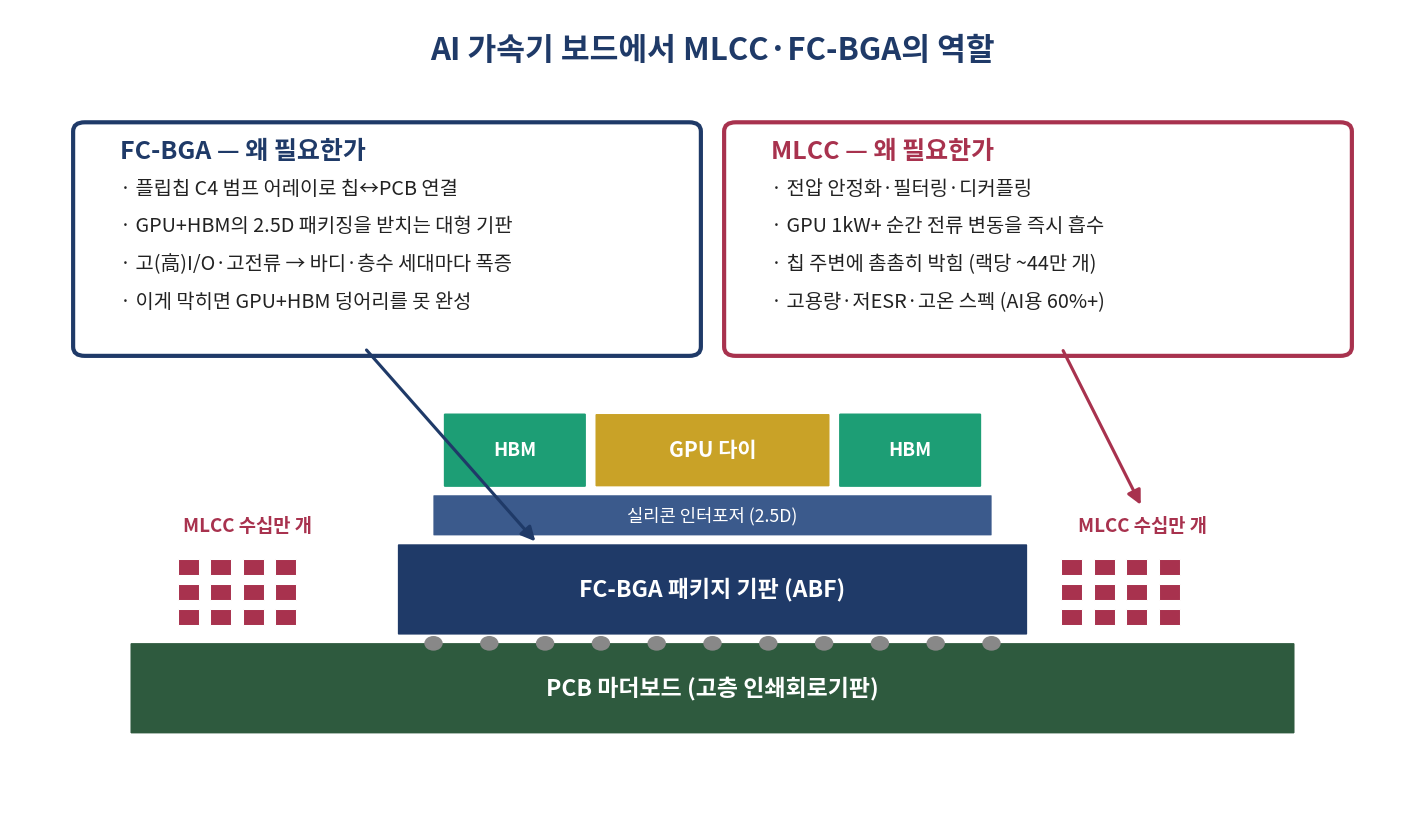

Chart 1 — The role of MLCC and FC-BGA on an AI accelerator board. Source: industry technical materials and USPTO patents

MLCC is a passive component that stabilizes circuit voltage, filters noise and replenishes current instant by instant. In an AI accelerator this role is decisive because of power. A single GPU draws over 1kW. When GPU, CPU, memory and network chips all run at high load together, current swings violently. The MLCC absorbs those instantaneous swings right next to the chip to keep voltage steady. The higher the power density, the more densely and abundantly they must be packed around the chip.

FC-BGA is the ultra-fine pedestal that links the chip to the mainboard (PCB). The flip-chip approach arrays bumps (C4 solder balls) across the entire underside of the chip to connect a high pin count over short paths. AI accelerators stack the GPU die and (high-bandwidth memory) on a silicon interposer in a 2.5D package (CoWoS); the FC-BGA substrate carries that whole block. As chips grow and I/O rises, the substrate grows larger and adds layers.

MLCC is the dam that feeds power steadily into the GPU; FC-BGA is the pedestal that connects the GPU-plus-HBM block to the PCB. Both are small in the bill of materials (BOM). But without them the other 99% — GPU and memory — stops.

How big it gets — content, value, market size

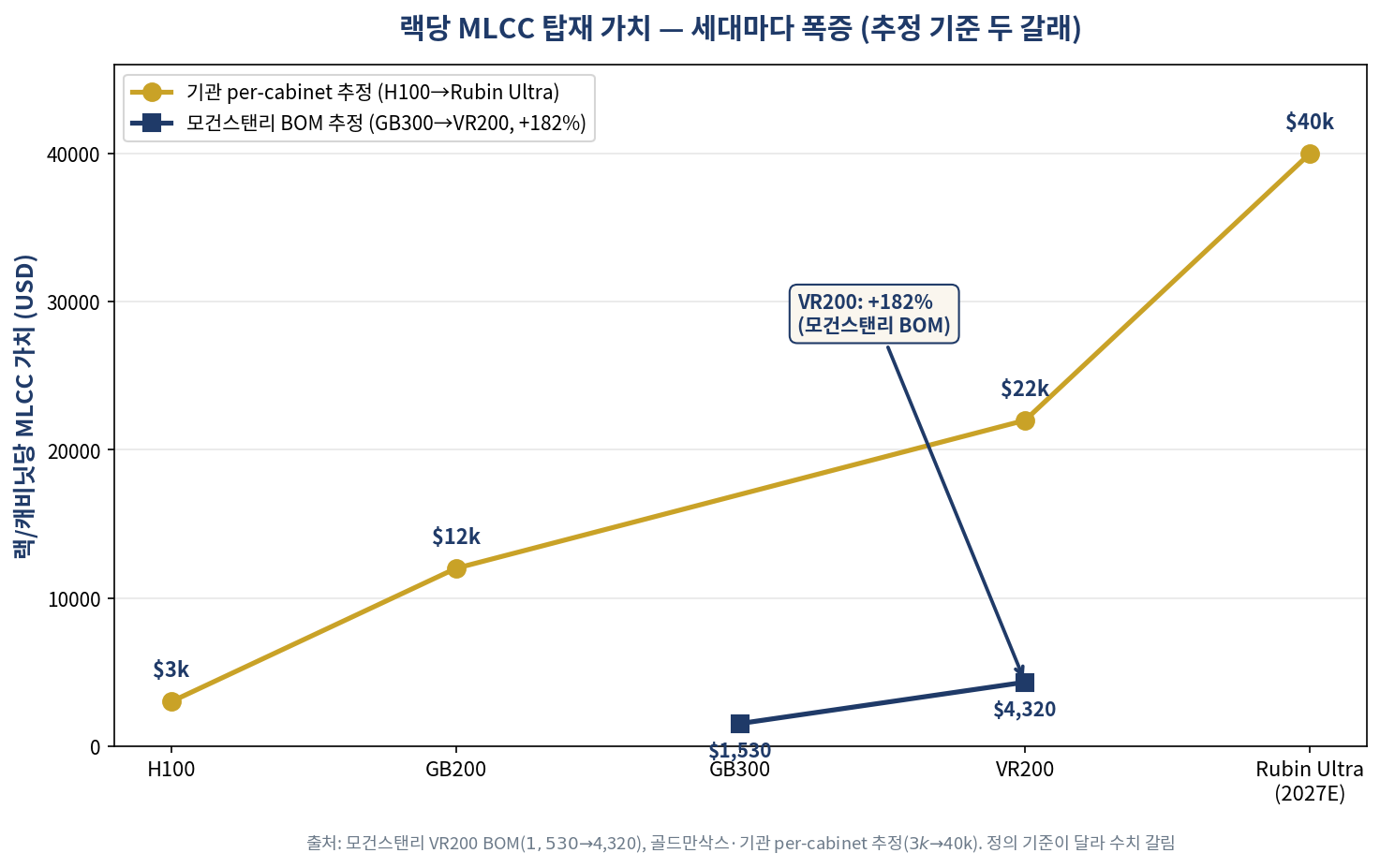

Start with content. A typical enterprise server holds about 1,000 MLCCs. A single Nvidia GB200 NVL72 rack needs about 440,000 — roughly 30x a smartphone. For AI servers, high-capacitance (10μF+), low-ESR models make up over 60% of the total. These high-spec parts are the very epicenter of the shortage.

Chart 2 — Generational increase in MLCC content value per rack. Source: Morgan Stanley, Goldman Sachs (different definitions)

Value growth splits into two estimates by source. On Morgan Stanley's BOM basis, the next-gen VR200 NVL72 rack's MLCC value is about $4,320, up 182% from the prior GB300's roughly $1,530. Goldman Sachs and other houses estimate per-cabinet value rising from about $3,000 for H100 to about $12,000 for GB200 and about $22,000 for VR200, exceeding $40,000 with Rubin Ultra in 2027. Definitions differ so absolute figures diverge — but the direction, an explosion each generation, agrees.

FC-BGA follows the same path. As AI accelerators grow each generation, substrate layer counts rise from 4 to 8-9 and then 16; above 14 layers is reserved for the most advanced accelerators and demands sub-30μm fine pitch. Package area exceeds 3,800mm² in CoWoS-L. Samsung Electro-Mechanics' 2026 FC-BGA revenue is estimated at KRW 1.7tn, up 45.5% year over year, reflecting this trend.

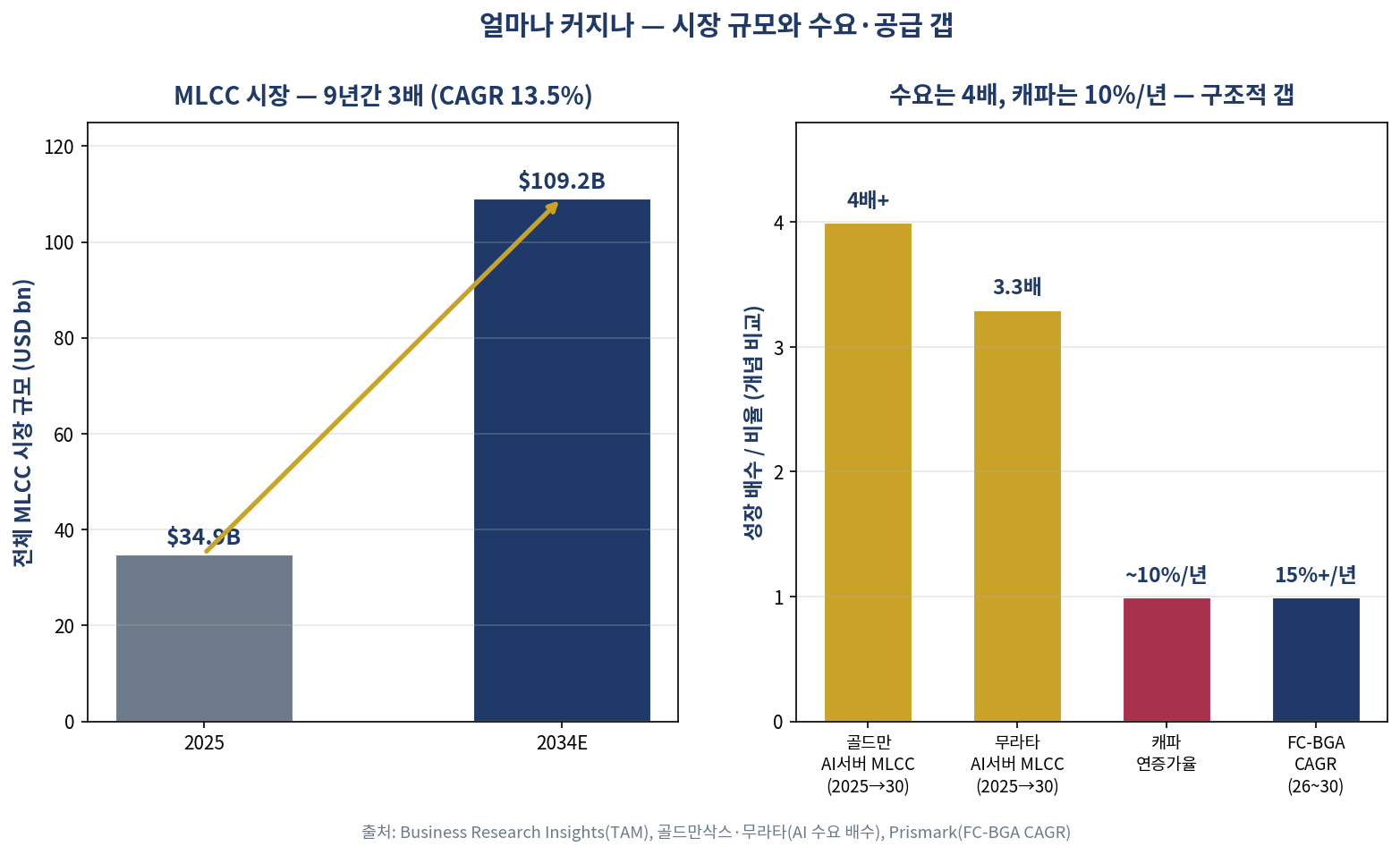

Chart 3 — Market size and the demand-supply gap. Source: Business Research Insights, Goldman Sachs, Murata, Prismark

On market size, the total MLCC market is estimated to grow from about $34.9bn in 2025 to about $109.2bn in 2034, a 13.5% CAGR. More important is the AI-server gap. Goldman Sachs sees AI-server MLCC demand rising more than 4x from 2025-30; Murata sees 3.3x of 2025 by 2030. Industry capacity grows only around 10% a year. The FC-BGA market, on Prismark's basis, grows over 15% a year from 2026-30 — the highest growth rate within the PCB industry.

Demand heads to 4x while capacity grows only ~10% a year. This gap is the root driver of the pricing cycle.