Reading depth

- Why we could bet on memoryThe thesis was a pattern continuation, not a forecast.Jump to section

- Memory is the pickaxe — 1849 reduxPickaxe prices are not the cycle's terminus. They are the miners' urgency meter.Jump to section

- Why they pay up for memoryThe price they pay reveals the prize they are chasing — and how far it sits from today.Jump to section

- Where the real bottleneck satMemory is one bottleneck. GPU is another. Neither has cleared.Jump to section

- The real shape of this gamePickaxes only sell while the miner is alive.Jump to section

- So peak debate is prematureCalling memory's peak now is premature. The end is set not by pickaxe (memory) prices but by the miners' (hyperscalers') capex and funding environment.Jump to section

Why we could bet on memory

Where this memory cycle ends, no one knows. I don't either. Calling cycle peaks is always a backward exercise.

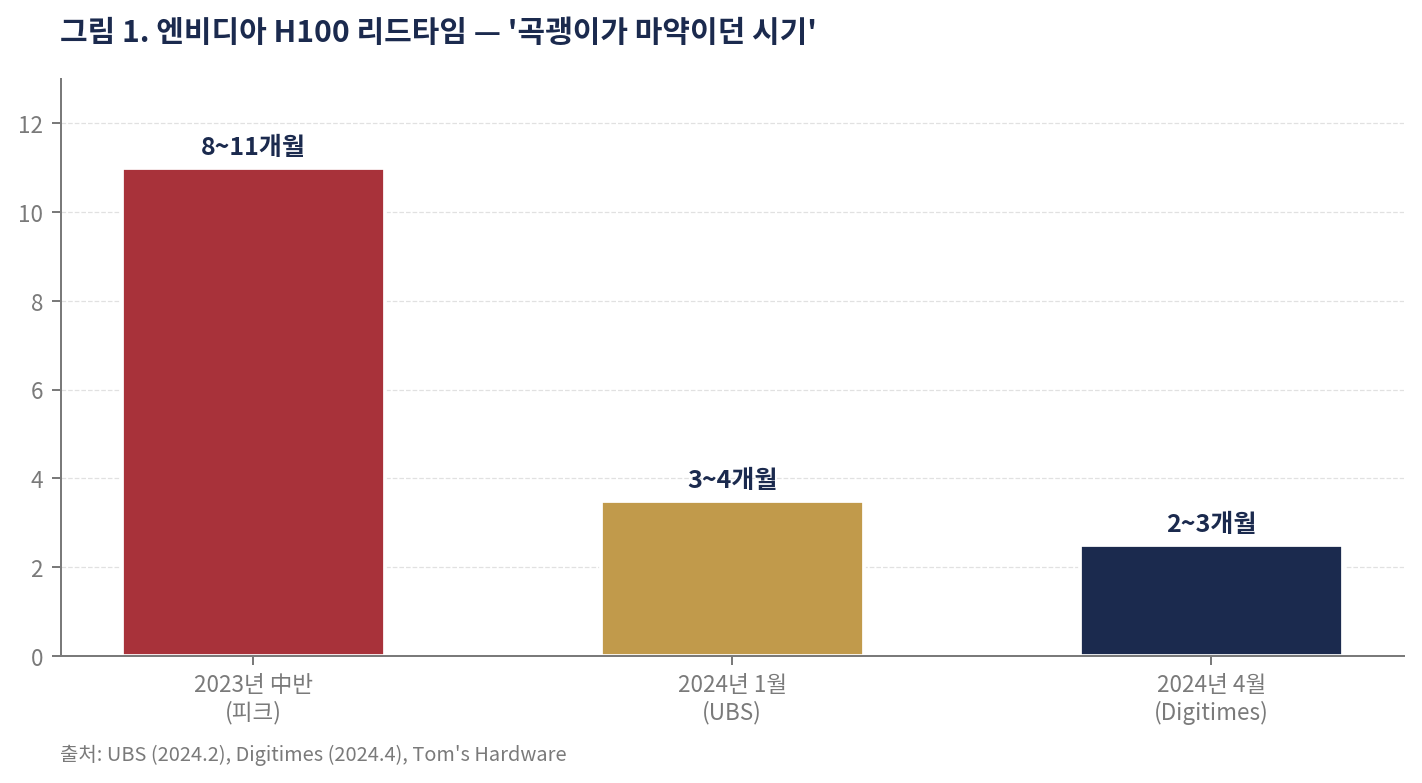

But betting on memory wasn't about predicting the future. It was about extending the past. We saw it once already, in 2023 and 2024. NVIDIA H100 lead times stretched 8 to 11 months. Some orders waited 40 weeks or more. China-bound A800 and H800 traded at a 40% premium over list, with six-month-plus queues. The joke that GPUs were harder to score than narcotics wasn't really a joke.

H100 lead times reached 8-11 months mid-2023. They normalized sharply through 2024.

What sat next to the GPU, who made it, who got paid for it — that part was obvious. The memory bet wasn't a forecast. It was an extrapolation. There was no reason what happened to GPUs wouldn't happen to memory.

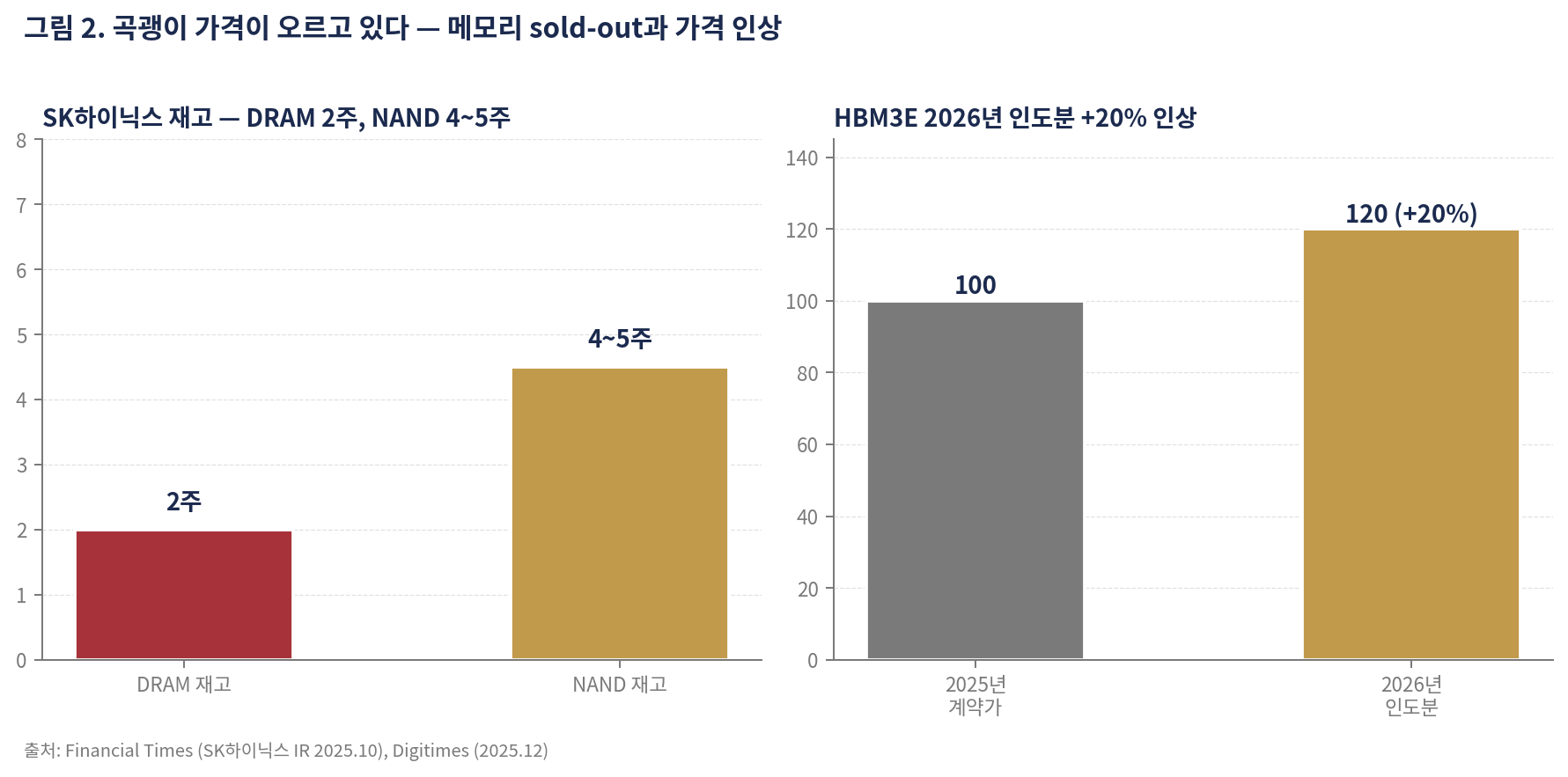

It is happening, exactly. SK Hynix's DRAM marketing chief told the FT in October 2025 that next year's DRAM, NAND, and capacity was sold out. At the same time SK Hynix DRAM inventory dropped to about two weeks. Some DDR5 SKUs hit zero inventory and shipped straight from production. The Korean memory duo raised 2026 HBM3E delivery prices by roughly 20%.

Inventory at multi-year lows. Prices up double digits.

The GPU drug story is rerunning, frame by frame, on memory. From here, opinions split. How much memory is really needed depends on how deep your AI thesis runs. Some saw a shortage. Some saw a structural surge. Same ticker, different conviction.

The thesis was a pattern continuation, not a forecast.