PSK Holdings is the only Korean equipment maker supplying Memory 3 + TSMC simultaneously, while breaking Japan ULVAC's 30-year Descum monopoly in HBM and CoWoS back-end. The alpha the market has missed is real (Reflow per CoWoS capacity = 6× HBM, 35% non-Korea revenue, 60+ global customers) — but the company's own 2026–2030 OPM ≥20% guidance signals it sees cycle-peak passage as a real possibility, and both sides need to be held in view.

Reader's Brief — 30-second TL;DR

Advanced

Why Now

Q2–Q3 2026 earnings — verify CoWoS Reflow share within revenue decomposition. TSMC CoWoS capacity progress: 2025 40K/M → 2026 90K/M. HBM4 16-Hi mass production ramp activating the 2.7× TSV effect. Korea Investment Securities target: KRW 160,000 (+22%).

This chapter is a primer for readers with no semiconductor background. Anchoring the industry structure first makes the deep dive much easier to absorb.

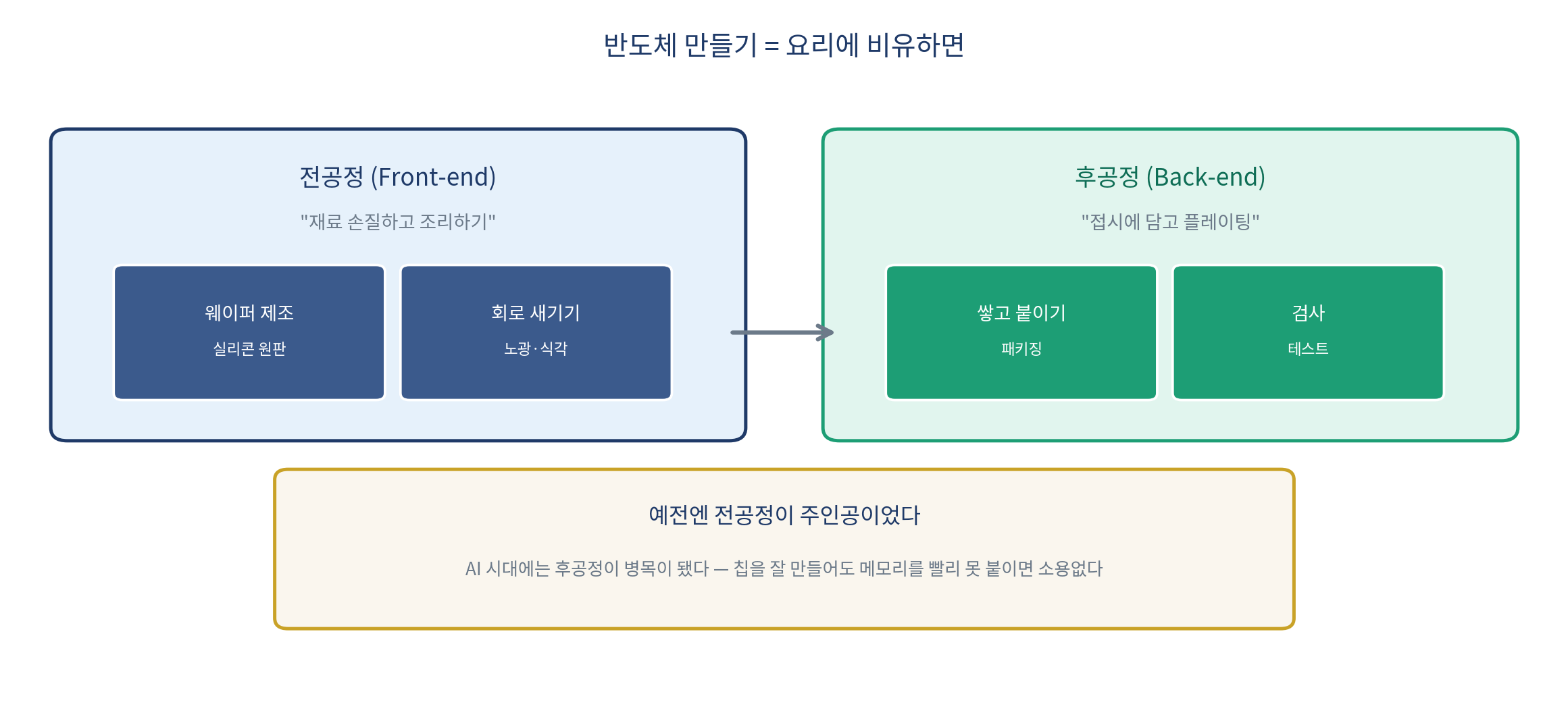

Front-end vs back-end — a cooking analogy

manufacturing splits into two halves: front-end and back-end.

<Figure 0-1> Front-end vs back-end

Front-end is the prep and cooking. Etching circuits onto a clean silicon wafer. The 7nm / 5nm / 3nm headlines you hear all live in this stage — the race to print smaller circuits.

Back-end is the slicing, stacking, bonding, and packaging of finished chips. In cooking terms: plating. Packaging and testing belong here.

Front-end used to be the protagonist. Then AI changed the script. However well you build a single chip, if memory next to it can't keep up, AI runs slow. Suddenly the back-end — stacking and bonding — became both the bottleneck and the prize. That is the layer PSK Holdings sits in.

The back-end has multiple stages

Back-end is not one step. It splits into many sub-processes, each dominated by a different equipment vendor.

<Figure 0-2> HBM back-end stages and dominant equipment makers

Stage 1 — drilling holes. HBM stacks 12 layers of DRAM. To pass electricity between layers, you drill microscopic holes ( — Through-Silicon Via) through each die. Lam Research and Applied Materials (US) dominate this etching step.

Stage 2 — residue cleanup. After drilling, polymer residue remains. Plasma cleaning removes it — this is . PSK Holdings' core product.

Stage 3 — solder ball flattening. The small solder bumps that bond chips need to be evenly flattened — that is . Also a PSK Holdings core product.

Stage 4 — stacking. Precisely stacking 12 layers of DRAM dies — Thermo-Compression Bonder (TC Bonder). Hanmi Semiconductor is the global #1.

Stage 5 — bonding GPU and memory on one substrate. Combining memory and GPU on a fine-line bridge called an interposer — CoWoS. TSMC owns this.

Key point: PSK Holdings makes money at Stage 2 (Descum) AND Stage 3 (Reflow) — two adjacent processes, not one. That dual-process footprint is the starting point of this report's multi-exposure thesis.

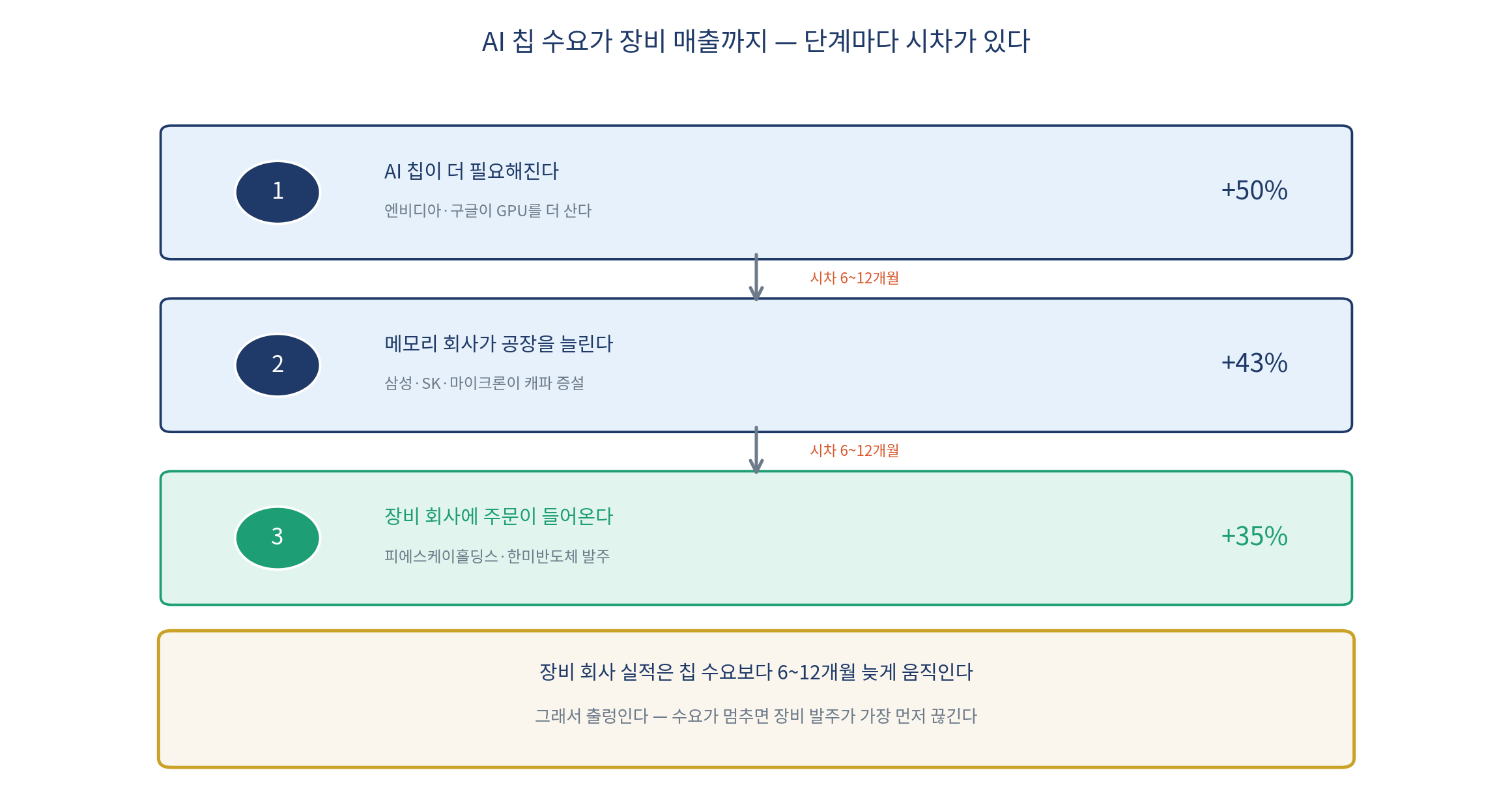

How equipment makers actually earn revenue

Critical investing concept: "If AI chip demand rises, doesn't the equipment maker automatically win?"

<Figure 0-3> The lag from AI chip demand to equipment revenue

Answer: yes, with a lag. Nvidia or Google buying more GPUs prompts memory makers (Samsung, SK Hynix, Micron) to evaluate fab expansions. Only after that decision do equipment orders flow. This chain typically runs 6 to 12 months.

That lag is the essence of equipment-stock behavior. Even when chip demand spikes, if memory makers hesitate, orders slip. Equipment revenues run 6 to 12 months behind chip demand, and quarterly results swing accordingly.

The reverse holds too. When demand stalls, equipment orders cut off first. Chips keep flowing from existing fabs, but new equipment purchases stop. That is why equipment stocks fall earliest at cycle peaks.

Carry this lag concept forward — it makes the quarterly swings (record Q4 2024 → Q2 2025 disappointment → recovery) we discuss later self-explanatory.

Full access requires a free account

Sign in with Google to unlock the full body of every free report instantly.

This site runs on ads — the tier system rewards community contributions.

Comments

This report is provided for informational purposes only and does not constitute a recommendation to buy or sell any financial instrument. Investment decisions should be made based on your own judgment and responsibility. The analysis and opinions contained herein are based on information available at the time of writing and are subject to change.