Samsung Electro-Mechanics is the only Korean company exposed to all three exploding data-center BOM items — MLCC, ABF substrate, glass substrate. The thesis is clear, but at ~73x 2027 estimated earnings (3.6x peers at ~20x), being a good company and being a good price now are two different things. The answer is Yes, but.

Reader's Brief — 30-second TL;DR

Intermediate

Why Now

Q1 2026 topped KRW 3tn in quarterly revenue for the first time (KRW 3.209tn revenue, KRW 280.6bn operating profit), driven by AI-server/automotive MLCC and AI-accelerator/CPU FC-BGA. A May target-price upgrade rush (Mirae Asset KRW 1.3M, SK KRW 2.0M, KB KRW 2.2M).

Winners ?? Losers

Multi-exposure — only Samsung Electro-Mechanics holds all three axes: MLCC (Component), FC-BGA (Package Solution), glass substrate. Single-exposure — Murata (MLCC only), Ibiden (ABF only). The axes sit at different cycle points (MLCC price-start, FC-BGA 2H shortage, glass 27~28 ramp), so as one peaks the next takes over.

Watch For

MLCC price-hike cycle progress, FC-BGA 2H-2026 shortage utilization/pricing, glass-substrate Sejong pilot and Sumitomo JV ramp schedule, any slowdown in the AI-server investment cycle, and the burden of a 73x 27F PER.

Why Samsung Electro-Mechanics — A Logic That Starts From the BOM

This report's logic does not start with the stock. It starts with the cost structure the AI server: first see which components grow structurally, then go find the Korean company that makes the most of them.

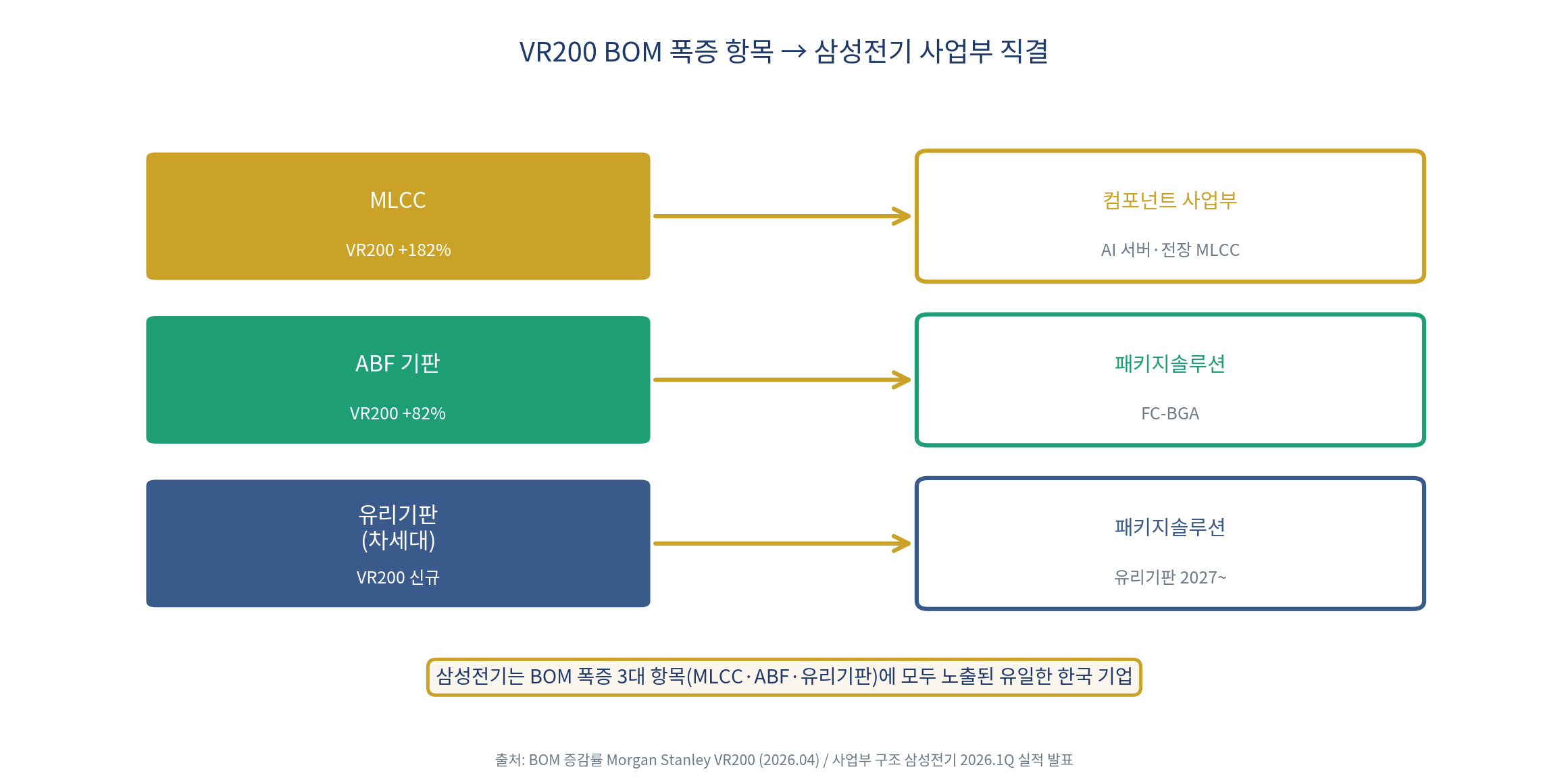

<Chart 1> How the exploding VR200 BOM items connect directly to Samsung Electro-Mechanics' divisions

Three signals the BOM revealed

In Morgan Stanley's VR200 NVL72 rack BOM analysis, memory grew the most at +435% versus GB300. But the very next line held meaningful items: PCB +233%, +182%, ABF +82%. Their absolute BOM share is under 2%, yet their growth is second only to memory.

This matters because BOM share and bottleneck intensity are different things. An item with small share but fast growth — one without which the whole system stops — is easy for the market to underrate by looking at share alone. MLCC and ABF substrate sit exactly there.

All three signals point to Samsung Electro-Mechanics

Connect these three items to Korean companies and they converge on Samsung Electro-Mechanics. MLCC is the core product of its Component division — a global No. 2 behind Japan's Murata. ABF substrate (, flip-chip ball grid array) is made by its Package Solution division: high-value substrates for AI accelerators and server CPUs.

Add next-generation glass substrate, also under development in the Package Solution division, targeting 2027~2028 mass production. In short, Samsung Electro-Mechanics is the only Korean company exposed to all three exploding BOM items (MLCC, ABF substrate, glass substrate).

Compared with other Korean firms, the rarity of this multi-exposure is clear. High-layer PCB is handled by Daeduck and Isu Petasys, SOCAMM substrates partly by Simmtech, Korea Circuit, and TLB — but the only Korean firm holding both MLCC and FC-BGA among the global leaders is Samsung Electro-Mechanics. Unlike Murata (MLCC only) and Ibiden (ABF only), it does both.

Samsung Electro-Mechanics is the only Korean company exposed to all three exploding BOM items — MLCC, ABF, and glass substrate. That multi-exposure is the basis for calling it the top Korean component pick.

Full access requires a free account

Sign in with Google to unlock the full body of every free report instantly.

This site runs on ads — the tier system rewards community contributions.

Comments

This report is provided for informational purposes only and does not constitute a recommendation to buy or sell any financial instrument. Investment decisions should be made based on your own judgment and responsibility. The analysis and opinions contained herein are based on information available at the time of writing and are subject to change.