Bottom Line

A triple capacity-expansion cycle (TSMC + memory big-three + supply chain) kicks in 2026–2028. Korean and Japanese suppliers with 50%+ category share capture revenue-proportional upside.

TSMC 2nm + simultaneous memory big-three expansion + the suppliers' triple order cycle

A triple capacity-expansion cycle (TSMC + memory big-three + supply chain) kicks in 2026–2028. Korean and Japanese suppliers with 50%+ category share capture revenue-proportional upside.

TSMC's 5 N2 fabs, SK hynix Cheongju P&T7, and Samsung Pyeongtaek P4 Ph4 all converge on 2026 ramp. Foundry, memory, and advanced packaging — historically out of sync — activate simultaneously for the first time.

Winners — KR (Hanmi Semi · HPSP · Intekplus · Isu Petasys), JP (DISCO · TEL · Shin-Etsu · JSR · Resonac), Global (BESI). Pressure — Hanwha Semitech's encroachment on Hanmi's TC bonder share at SK hynix.

Quarterly hyperscaler CapEx guidance from MS, Google, Meta, Amazon. Continued upgrades = cycle extends; first downgrade = peak signal. Next checkpoint: 26Q1 earnings.

****

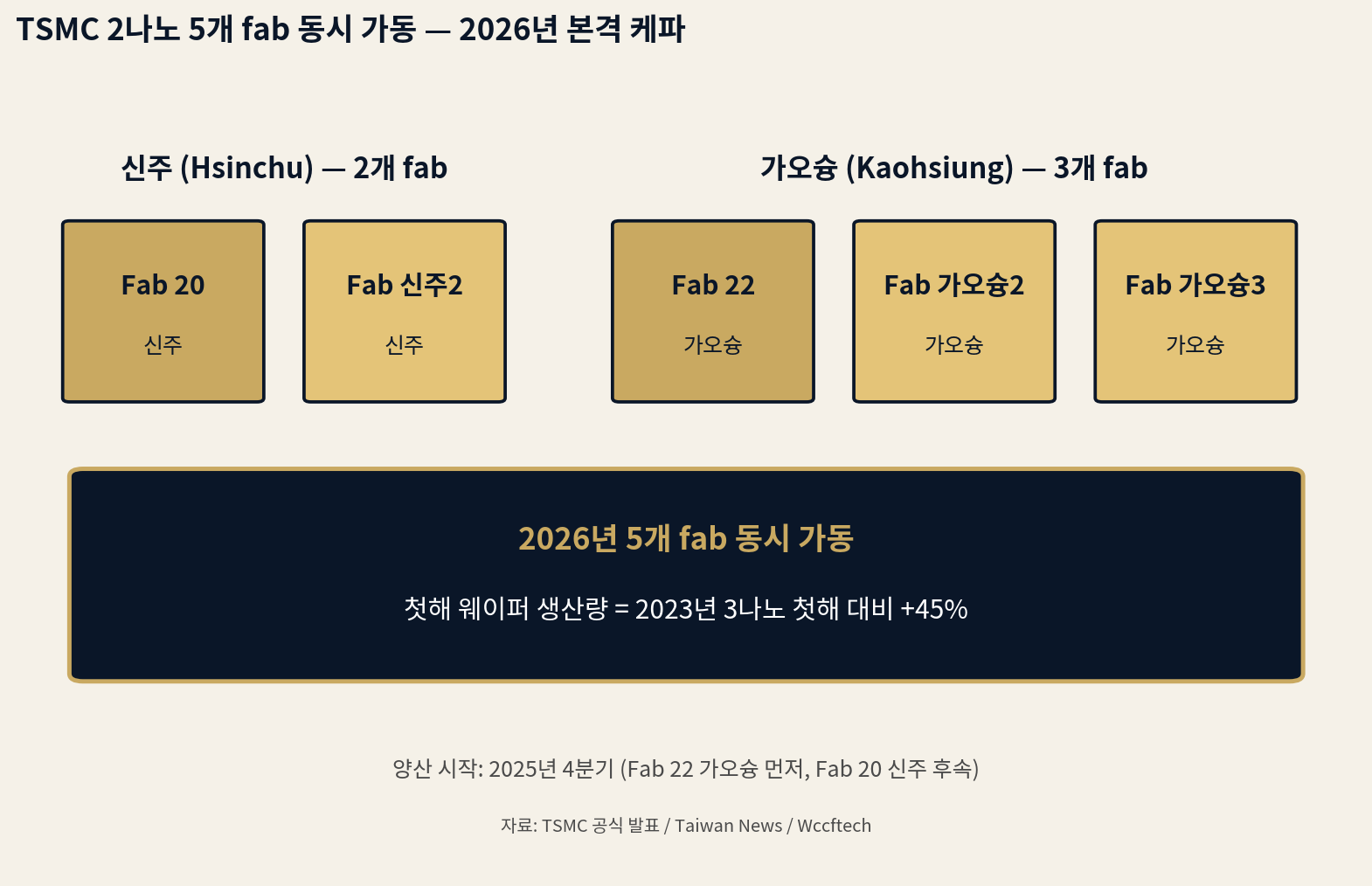

[Figure 1] TSMC's five 2nm fabs running simultaneously — full capacity in 2026

TSMC 2nm (N2) volume production started at Kaohsiung Fab 22 in Q4 2025 and enters full capacity expansion in 2026. The five fabs running in 2026 are Fab 20 and Hsinchu 2 (adjacent to R&D) in the Hsinchu cluster, plus Fab 22, Kaohsiung 2, and Kaohsiung 3 in the Kaohsiung cluster. First-year wafer output at +45% versus the 2023 first year of 3nm matters a great deal — it signals that TSMC is investing in 2nm capacity far more aggressively than it did at the 3nm introduction.

The direct driver of this acceleration is AI accelerator demand. With NVIDIA's Vera Rubin architecture adopting the 2nm + HBM4 + -L combination, a single customer has pre-locked more than 50% of TSMC's 2nm capacity. AMD's MI400 series and the ASICs of AWS, Google, Meta, and Microsoft are converging on 2nm as well. Five 2nm fabs running at once is not a single-scenario bet — it is a response to simultaneous demand surges from five to seven hyperscale players.

****

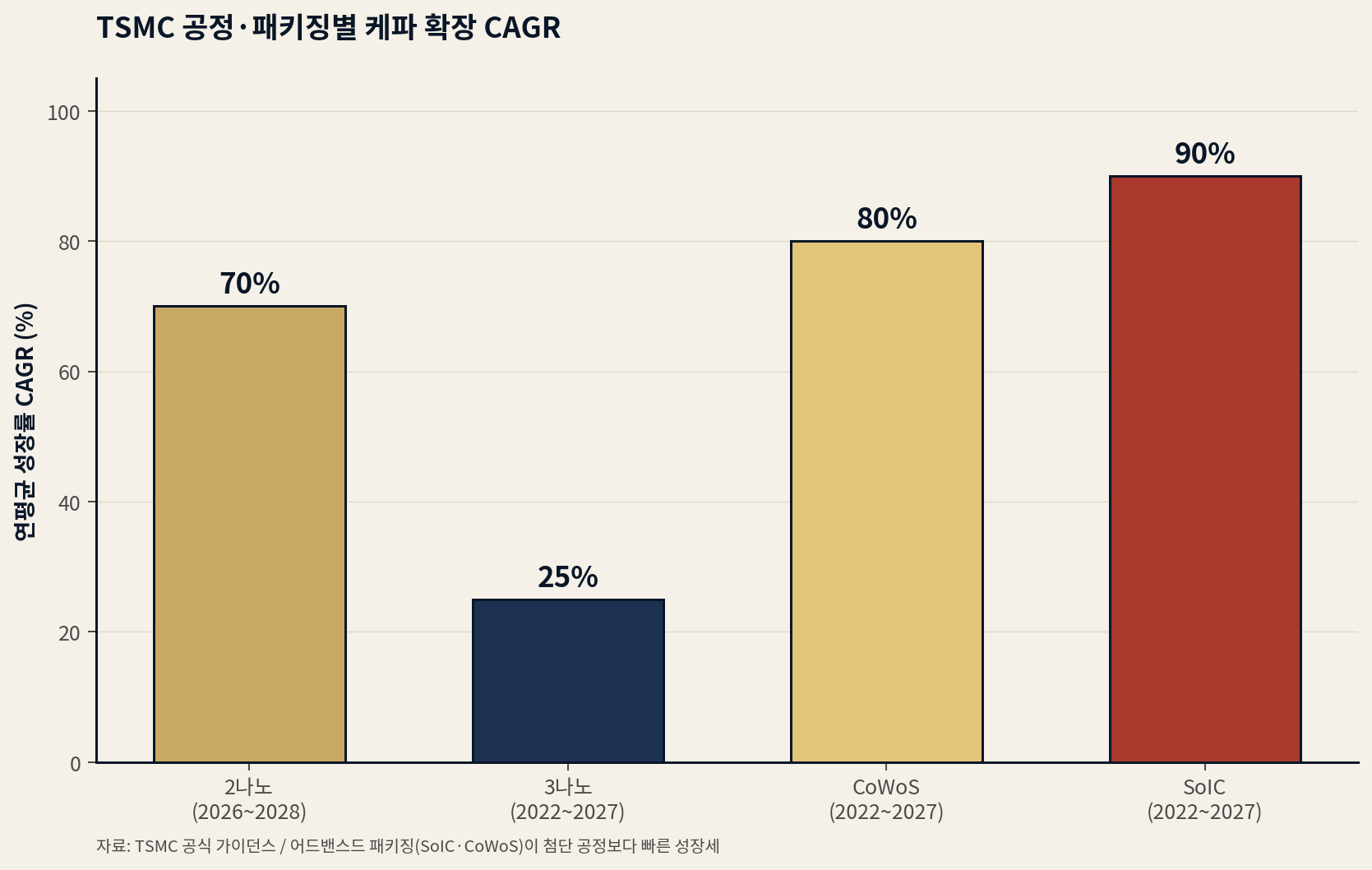

[Figure 2] TSMC capacity expansion CAGR by process and packaging

Comparing the capacity CAGRs TSMC has officially guided reveals a telling pattern. 2nm is very steep at a 70% CAGR for 2026–2028, but advanced packaging is faster. CoWoS runs at an 80%+ CAGR and SoIC at 90%+ over 2022–2027. 3nm grows at a 25% CAGR over the same period — roughly a third to a quarter of packaging's pace. The implication is clear — the fastest-growing area of the AI-era semiconductor value chain is not the leading-edge process but advanced packaging.

| Item | Period | CAGR | Meaning |

|---|---|---|---|

| 2nm capacity | 2026–2028 | 70% | Acceleration into full volume production |

| 3nm capacity | 2022–2027 | 25% | Stable growth in maturity |

| CoWoS capacity | 2022–2027 | 80%+ | Core of NVIDIA·AMD AI accelerators |

| SoIC capacity | 2022–2027 | 90%+ | Bound for NVIDIA Rubin·Feynman |

SoIC is steepest at 90%+ because NVIDIA's Rubin Ultra (2027) and next-generation Feynman (2028) architectures are set to adopt SoIC as their core packaging technology. SoIC uses copper-to-copper hybrid bonding for 3D vertical stacking, dramatically raising transistor density. per 10K wafers of SoIC capacity runs about $6.8–7.0B — far more capital-intensive per unit of capacity than CoWoS. A 90% SoIC CAGR combined with that capital intensity creates the largest order surge in the entire advanced-packaging equipment market.

****

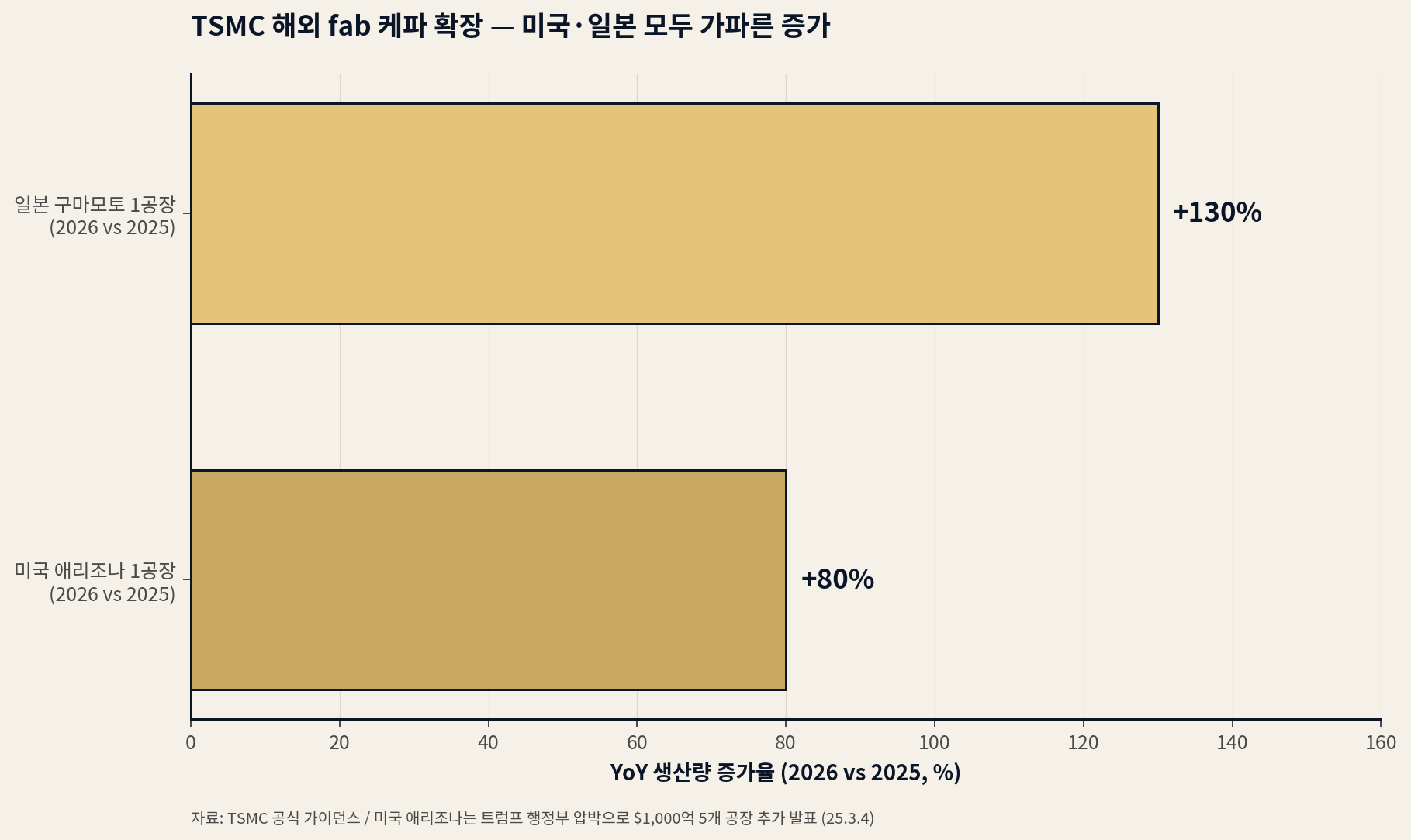

[Figure 3] TSMC overseas fab capacity — steep growth in both the US and Japan

2026 is the inflection point for TSMC's overseas fab expansion. Arizona Fab 1 output rises +80% in 2026 versus 2025; Kumamoto Fab 1 in Japan rises +130%. Add the additional $100B US investment (five more plants) announced on March 4, 2025 under Trump-administration pressure, and TSMC's US capacity traces its steepest cumulative growth curve over 2026–2030.

Overseas fab acceleration matters greatly for Korean and Japanese suppliers. Every new overseas TSMC fab brings global shipping, qualification, and localization of materials, parts, and equipment — and Korean suppliers (notably Hanmi Semiconductor and HPSP) and Japanese suppliers (notably DISCO and Tokyo Electron) already have proven global supply-chain relationships, making them direct beneficiaries of the revenue expansion. The Arizona advanced-packaging facility in particular ramps in earnest in 2027–2028, which makes 2025–2026 the window when its equipment orders concentrate.

Sign in with Google to unlock the full body of every free report instantly.

Sign in with GoogleThis site runs on ads — the tier system rewards community contributions.

This report is provided for informational purposes only and does not constitute a recommendation to buy or sell any financial instrument. Investment decisions should be made based on your own judgment and responsibility. The analysis and opinions contained herein are based on information available at the time of writing and are subject to change.