ChangXin Memory (CXMT) — The Price of the Listing Venue: Deconstructing China's DRAM Champion IPO

A record 57.9-billion-yuan STAR Market raise with a 6% day-one float by design — what sets the opening price is neither DRAM nor HBM but the listing venue itself. The premium expires in July 2027, when the lockups come off

The day-one price of China's DRAM champion IPO is a function of float scarcity, the A-share localization premium, and the memory supercycle narrative — not fundamentals. Roughly half of the 2-3 trillion yuan consensus is the price of the listing venue, not the price of the asset.

Reader's Brief — 30-second TL;DR

Advanced

Why Now

July 27 STAR Market listing confirmed — 8.66 yuan offer, 57.9B yuan raised (~66.6B with greenshoe), breaking SMIC's 2020 record. CXMT arrives with cycle-peak earnings: Q1 revenue up 719% and first-half profit guidance of 50-57 billion yuan.

Winners ?? Losers

Near term it does not impair the Korean big three's cycle logic — while CXMT absorbs commodity demand, the three accelerate their high-value mix shift. Non-US equipment and materials gain $5-6B of derived procurement demand. The pressure arrives after 2028 — a supplier outside the production-cut cartel holding 17% of global DRAM supply.

Watch For

An opening below 2 trillion yuan (A-share fervor cooling) or above 3 trillion (overheating), whether the Hyperliquid pre-IPO perp premium holds or compresses (near $8.0 as of July 15, an implied cap of about 3.8 trillion yuan — above the consensus ceiling) along with its open-interest growth, and whether strategic-placement institutions publicly commit to holding in the months before the July 2027 lockup cliff.

Reading depth

Eight Years of Losses, One Half-Year Reversal

ChangXin Memory, founded in 2016 in Hefei, Anhui province, is China's largest DRAM maker. It runs three 12-inch DRAM fabs across Hefei and Beijing and has extended its lineup through DDR5 and LPDDR5, ranking fourth globally in DRAM with roughly 8% revenue share. Founder and chairman Zhu Yiming also founded the NOR flash and MCU company GigaDevice. A Tsinghua graduate, he filled China's DRAM void through a joint venture with the Hefei municipal government.

A dramatic financial reversal is the backdrop to this . From 2016 to 2024 the company accumulated roughly 36.6 billion yuan of losses while ramping capacity, with long-term borrowings reaching 118.8 billion yuan. Then in the first quarter of 2026 it swung abruptly into the black: revenue of 50.8 billion yuan (up 719% year over year) and net profit attributable to shareholders of 24.76 billion yuan (up 1,688%). The company's guidance for the first half of 2026 is revenue of 110-120 billion yuan and attributable net profit of 50-57 billion yuan. That pace effectively erases eight years of accumulated losses with a single half-year of earnings.

Two forces overlapped to drive the reversal. First, the AI-driven memory supercycle. As the global top three concentrated capacity on HBM and server DRAM, a supply vacuum opened in commodity DRAM, and CXMT — centered on DDR4 and LPDDR — absorbed it, enjoying price and volume at once. Second, its own capacity reached economies of scale. Utilization climbed from 87% in 2023 to about 96% in 2025, and the workhorse node migrated to G4, roughly equivalent to the industry's 1z class.

Reservations about earnings quality must be stated. Current profits are leveraged to cycle-peak prices, and 99% of revenue comes from commodity DDR and LPDDR products. Overseas revenue is just 2.79% of the total; key customers are Chinese firms such as Alibaba Cloud, ByteDance, Xiaomi, and Honor. HBM contributes essentially no revenue yet. Its DDR5 parts are implemented by enlarging the die rather than shrinking the process, drawing criticism on cost and yield.

Governance is a textbook state-led capital structure: Hefei government investment platforms, the National IC Industry Investment (the "Big Fund"), bank-affiliated investment arms, and insurers form the skeleton. Chairman Zhu has pledged to sell none of his stake for ten years after listing, and for the following decade to dispose of at most 20% of the remainder per year. He also designed the largest personal-equity employee incentive in A-share history, distributing half of the 1.536 billion shares allotted to his partnership platform to employees over ten years.

CXMT is the case of an asset the state nurtured through eight years of losses arriving on the market timed precisely to the cycle peak. The 50-billion-yuan half-year profit is real, but more than half of it belongs to the cycle — that is where valuation must start.

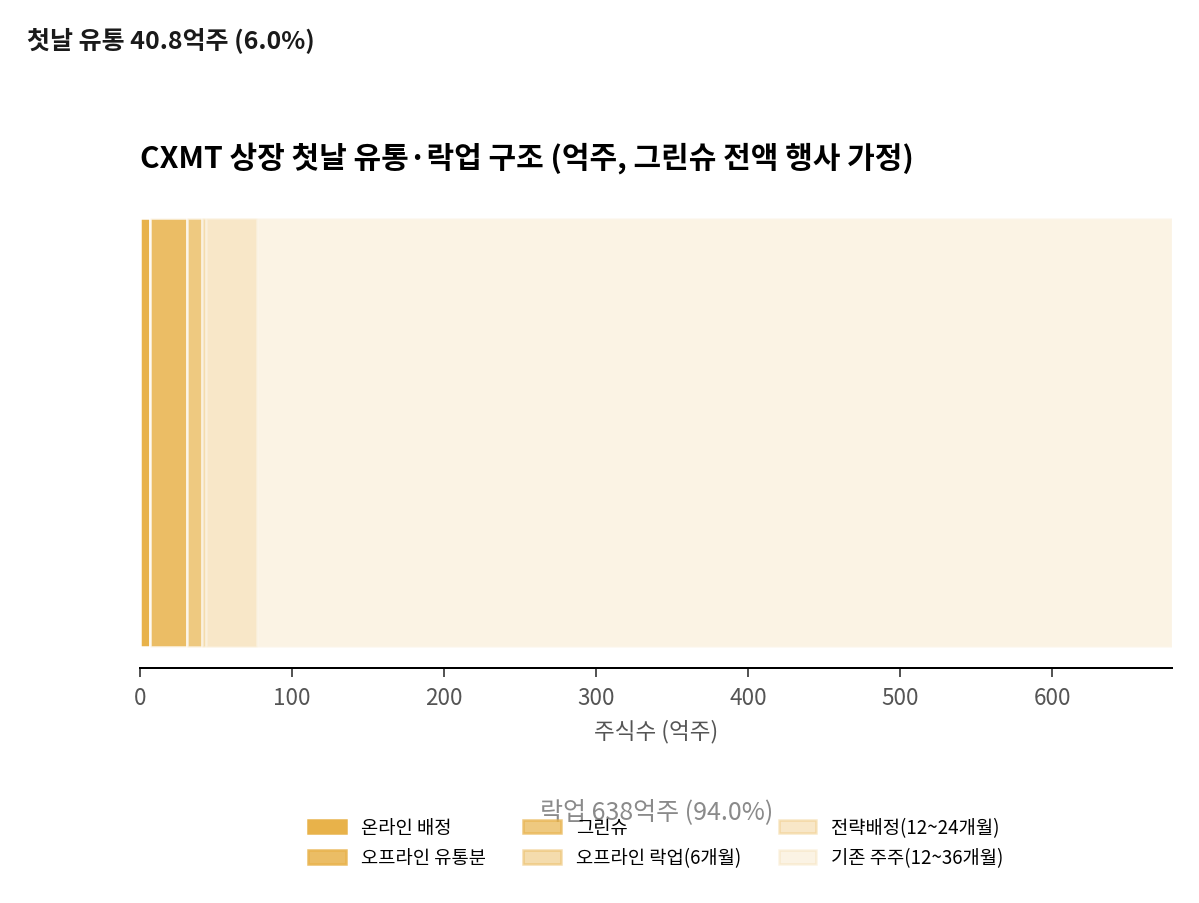

The 6% Float by Design — Offering Structure and Share Supply

The offering is a three-way structure: 50% strategic placement, 40% offline (institutional book-building), 10% online (retail). Of the 6.688 billion shares, 3.344 billion go to strategic investors, 2.675 billion to the initial offline tranche, and 669 million to the initial online tranche. Joint lead underwriters CSC Financial and CICC hold a 15% option.

Allocation tranche

Shares (bn)

Share of offering

Strategic placement

3.344

50.0%

12-24 months

Offline (institutional)

2.675

40.0%

6 months on a 10% lottery slice

Online (retail)

0.669

10.0%

None

Greenshoe (over-allotment)

1.003

+15.0%

None

Allocation tranche

Strategic placement

Shares (bn)

3.344

Share of offering

50.0%

Lockup

12-24 months

Allocation tranche

Offline (institutional)

Shares (bn)

2.675

Share of offering

40.0%

Lockup

6 months on a 10% lottery slice

Allocation tranche

Online (retail)

Shares (bn)

0.669

Share of offering

10.0%

Lockup

None

Allocation tranche

Greenshoe (over-allotment)

Shares (bn)

1.003

Share of offering

+15.0%

Lockup

None

Day-one tradable supply computes as follows. The online 669 million shares float in full. Under rules 10% of the offline allocation is subject to a six-month lockup lottery, leaving about 2.41 billion shares floating, plus the 1.003 billion greenshoe shares if exercised. The total is roughly 4.08 billion shares — 6.0% of the 67.88 billion total shares outstanding including the greenshoe. At the offer price the floating market cap is only about 35.3 billion yuan, roughly $5.2 billion.

The release schedule of the remaining 94% is the supply clock. Around January 2027, six months in, about 270 million offline lockup shares unlock — negligible. The decisive cliff is twelve months out, in July 2027, when the 3.344 billion strategic-placement shares and the 12-month lockups of existing financial investors (Big Fund II, Alibaba affiliates, GigaDevice, and others) release simultaneously. Controlling-shareholder blocks carry 36-month lockups, and Chairman Zhu's personal stake sits under his voluntary ten-year lockup.

Float jumps; first trigger for premium compression

Date

Jul 2029 (T+36M)

Unlocking holders

Controlling shareholders

Implication

Zhu's personal stake under 10-year voluntary lockup

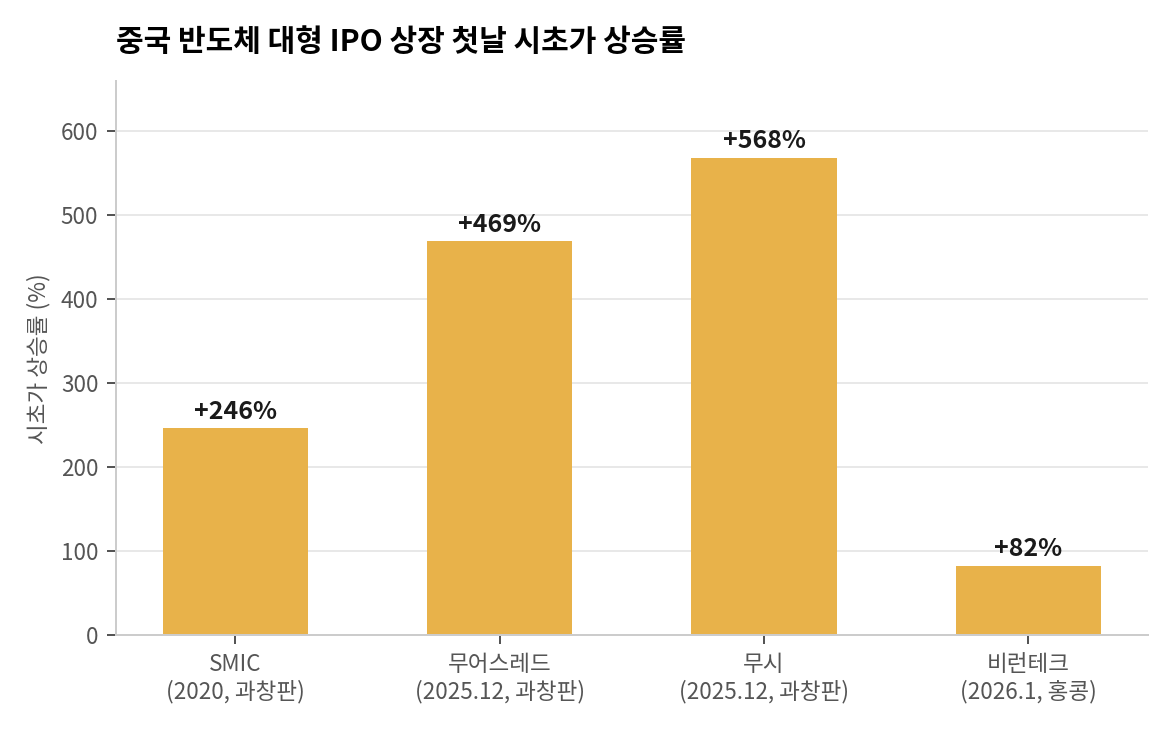

The 6% float is design, not accident. Large STAR Market IPOs have repeatedly used high strategic-placement ratios to compress the initial float and amplify demand through retail subscription contests. SMIC in 2020 likewise placed 50% strategically (29 institutions, 24.26 billion yuan) with a day-one float near 15% of shares outstanding — and the result was a 246% opening pop. CXMT's float ratio is even lower than SMIC's. On supply-demand alone, the structural conditions for a surge are stronger.

On day one, 4.08 billion shares — 6% of the company — will discover the price. That float compression is the supply-side foundation of the 2-3 trillion yuan consensus, and the July 2027 lockup cliff is the date on which the premium's decay is structurally pre-booked.

Rerunning the SMIC Script — STAR Market Precedents and Lockup Lessons

Large STAR Market semiconductor IPOs follow a stylized script: national strategic-asset status, a placement-heavy offering structure, a compressed initial float, and a several-hundred-percent day-one surge. CXMT's offering design is structurally identical to the 2020 SMIC original, and the market's temperature was proven by the domestic GPU listing rally of late 2025.

Opening-day gains of major Chinese semiconductor IPOs

Chart 2. Opening-day gains of major Chinese semiconductor IPOs (Source: listing announcements, press reports)

SMIC (July 2020) priced at 27.46 yuan — 109x earnings at issuance — yet opened at 95 yuan, up 245.96%, for a day-one market cap of 677.9 billion yuan. Its 53.23 billion yuan raise was then the largest in A-shares in a decade. Moore Threads (December 2025) priced at 114.28 yuan, opened up 468.78%, closed up 425.46%, and within six sessions touched 941 yuan for a 442.2 billion yuan market cap. MetaX followed twelve days later, opening up 568% and closing up 692.95% for a 332 billion yuan cap. Across the twelve STAR Market debuts of 2025, the average day-one gain excluding extremes was 266%.

Stock

Listed

Offer price (CNY)

Day-one open

Subsequent path

SMIC

Jul 2020

27.46

+245.96%

Day-one cap 677.9B yuan

Moore Threads

Dec 2025

114.28

+468.78%

~37% correction from peak

MetaX

Dec 2025

104.66

+568%

~35% correction from peak

Biren (H-share)

Jan 2026

-

+82%

Cap below HK$100B

CXMT

Jul 2026

8.66

?

Subject of this report

Stock

SMIC

Listed

Jul 2020

Offer price (CNY)

27.46

Day-one open

+245.96%

Subsequent path

Day-one cap 677.9B yuan

Stock

Moore Threads

Listed

Dec 2025

Offer price (CNY)

114.28

Day-one open

+468.78%

Subsequent path

~37% correction from peak

Stock

MetaX

Listed

Dec 2025

Offer price (CNY)

104.66

Day-one open

+568%

Subsequent path

~35% correction from peak

Stock

Biren (H-share)

Listed

Jan 2026

Offer price (CNY)

-

Day-one open

+82%

Subsequent path

Cap below HK$100B

Stock

CXMT

Listed

Jul 2026

Offer price (CNY)

8.66

Day-one open

?

Subsequent path

Subject of this report

Two regularities emerge. First, the size of the pop scales with float compression and narrative strength, not fundamentals. Moore Threads and MetaX were both loss-making, yet the domestic-GPU narrative and subscription allotment rates around 0.03% produced 400-700% openings. Second, a 30-40% correction after the surge is the standard path. Both names corrected roughly 37% and 35% from their peaks within a month of listing. The day-one price is not an equilibrium price but the product of a liquidity event, and price is rediscovered over the following weeks as the non-locked float changes hands.

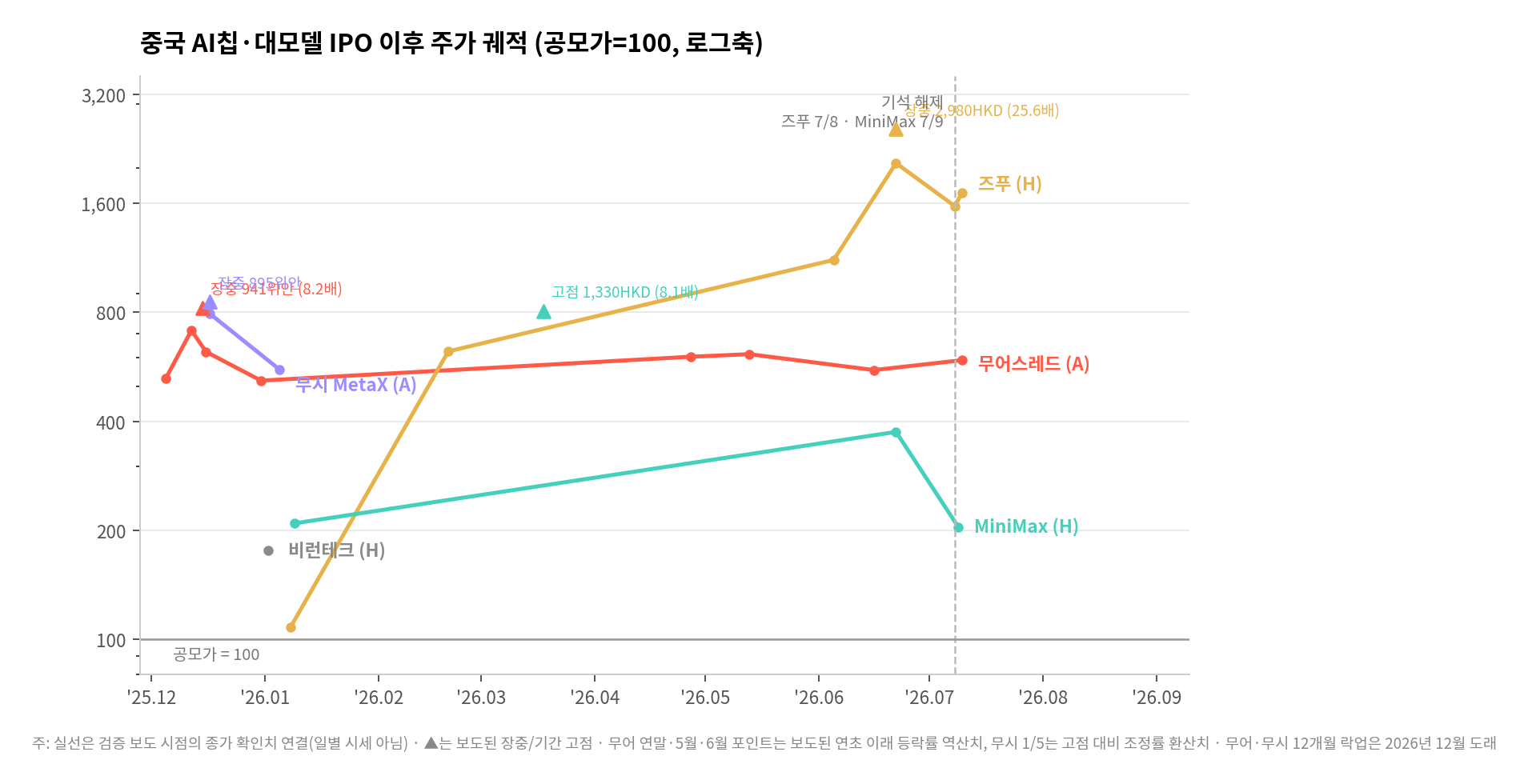

Post-Listing Trajectories and the Lockup Playbook

Extending the precedents from day one through lockup expiry yields three trajectory patterns. The chart below indexes five recently listed Chinese AI-chip and large-model companies to their offer price (offer = 100), connecting closes verified in press reports.

Price trajectories of Chinese AI-chip and large-model IPOs

Chart 3. Price trajectories of Chinese AI-chip and large-model IPOs, offer price = 100, log scale; solid lines are verified or back-computed closes, triangles are reported peaks (Source: filings, press reports)

The first pattern is the A-share GPU type. Moore Threads hit 8.2x its offer price intraday (941 yuan) within ten days, corrected about 37% from the peak within a month, then spent half a year in a box roughly 15% either side of the 5-6x zone (about 590-700 yuan). It bounced on a surprise first-quarter profit in late April, but by mid-June its year-to-date gain was just 6.8%, badly lagging the semiconductor rally — expectations front-loaded into the opening print still ran ahead of the pace of profit delivery. MetaX traced the same shape. The decisive fact: this correction happened without any lockup release. Both companies' 12-month lockups only mature in December 2026; the churn of day-one float alone erased a third of the peak. The day-one peak is a liquidity-event artifact; the meaningful baseline is not the peak but the plateau that follows.

The second pattern is the Zhipu type — a melt-up on extreme float compression. Zhipu, a large-model company listed in Hong Kong, gained only 8.4% on day one, but on a free float of 2.67% climbed as much as 25x its offer price over six months (HK$2,980 intraday, HK$1.3 trillion market cap). The July 8 cornerstone unlock (about 6% of shares outstanding) never became the feared cliff, because state-backed cornerstones holding about 70% of the unlocking shares publicly committed in advance to keep holding. The stock closed up 13.4% on unlock day, and the next day the company even placed new shares at that price level.

The third pattern is the MiniMax type — where the unlock triggered the repricing. MiniMax, also in Hong Kong, opened more spectacularly at +109% and reached 8.1x its offer price on March 18, then slid. On July 9 its unlock covered 34% of shares outstanding, much of it held by financial investors with strong incentives to sell; the stock fell more than 20% intraday, returning to roughly 2x the offer price — effectively its day-one close. Peak-to-trough, about 75%. Two companies with the same narrative diverged on unlock day on exactly one variable: who owned the unlocking shares. Biren, for reference, shows the control case — the same GPU story managed only +76-82% on day one in Hong Kong, and where no bubble forms, no correction follows.

Mapping the playbook onto CXMT: at a 6% float it sits structurally between Zhipu (2.67%) and the A-share GPUs, and as a profitable company its melt-up fuel is if anything richer. The base case immediately after listing should be the Moore Threads path — a day-one peak, a 30-40% correction within a month, then a plateau — and that correction arrives regardless of lockups.

Where CXMT differs from precedent, the difference strengthens the surge logic. Moore Threads and MetaX were prepayments on future earnings; CXMT arrives carrying present earnings of 50-plus billion yuan per half. An annualized P/E of 5-6x at the offer price is the lowest in the history of STAR Market semiconductor debuts — more than enough to trigger the retail intuition that it "came cheap." Why that intuition is wrong (the denominator problem of annualizing cycle-peak earnings) is covered in the valuation section, but in day-one price formation, intuition outruns analysis.

The STAR Market base rate: a +250-570% open, a 30-40% correction from the peak within a month (lockup-independent), then a plateau. Replaying SMIC (+245%) puts CXMT at 2.0 trillion yuan; replaying Moore Threads (+420%) puts it at 3.0 trillion — the precedent band reproduces the consensus band exactly.

Full access requires 🥉 Bronze tier

Sign in with Google — your tier will be checked automatically and access granted if eligible.

This site runs on ads — the tier system rewards community contributions.

Comments

This report is provided for informational purposes only and does not constitute a recommendation to buy or sell any financial instrument. Investment decisions should be made based on your own judgment and responsibility. The analysis and opinions contained herein are based on information available at the time of writing and are subject to change.