Bottom Line

Intel's Q1 earnings call was not just an earnings beat — it officially confirmed that the all-front shortage across HBM, CoWoS, ABF, and server CPU is structurally locked in through 2027-28.

CPU Renaissance · HBM/CoWoS/ABF Sold Out · ASIC Surge · Korean Value-Chain Exposure Map

Intel's Q1 earnings call was not just an earnings beat — it officially confirmed that the all-front shortage across HBM, CoWoS, ABF, and server CPU is structurally locked in through 2027-28.

The CFO's 'absolutely constrained' admission, the AWS-OpenAI $38B deal citing 'tens of millions of CPUs,' and TSMC CoWoS still sold out despite expansion to 125kwpm — three signals simultaneously quantified the supply ceiling.

Beneficiaries — HBM (SK Hynix, Samsung), CoWoS materials (Hanmi, HPSP), ABF substrates (Daeduck, Simmtech), server-CPU-linked memory. Pressure — foundry laggards unable to keep pace with demand expansion.

Quarterly TSMC CoWoS utilization rates and HBM contract pricing — the timing of supply-constraint relief is the key trigger for adjusting exposure in beneficiary names.

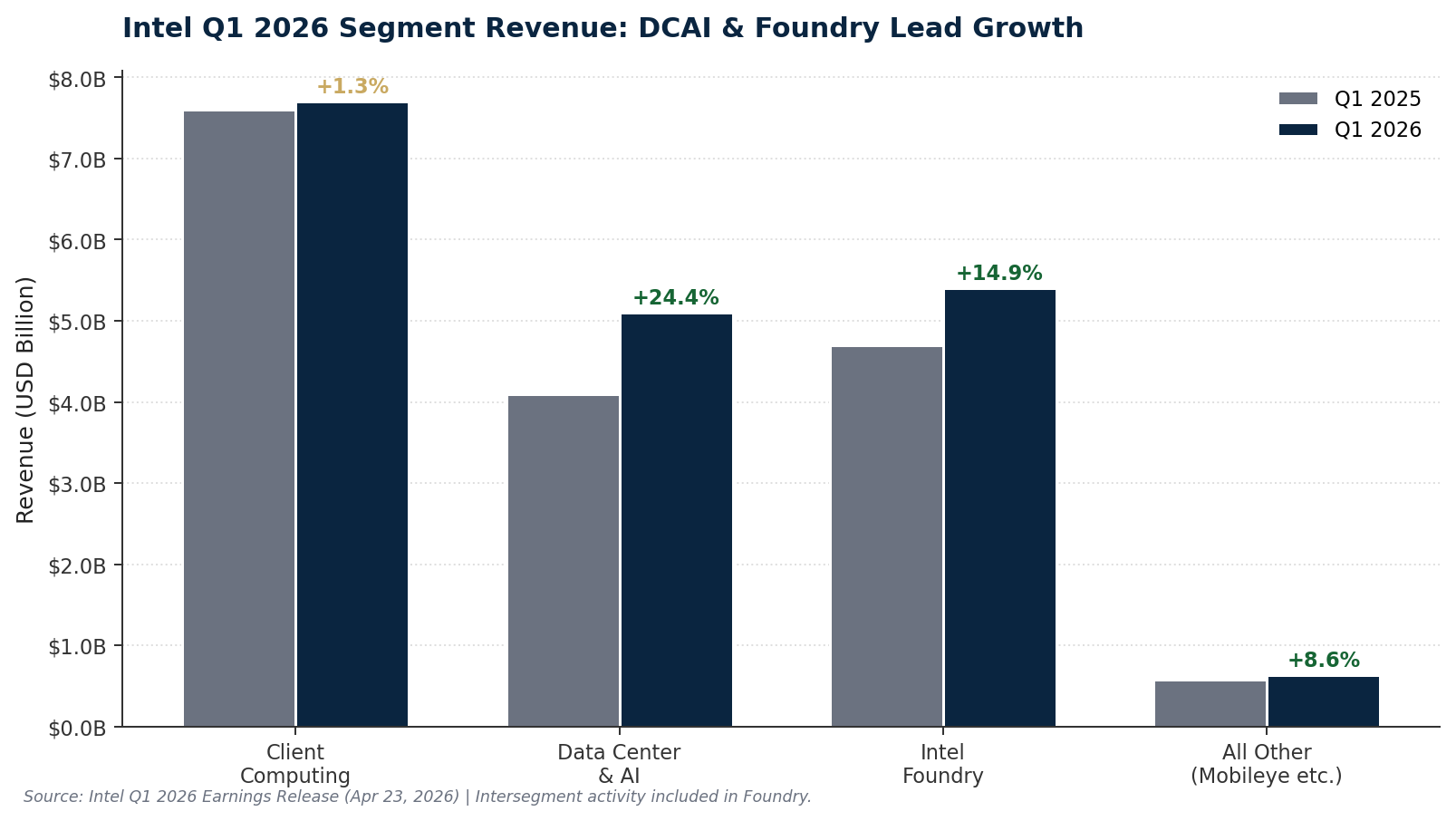

Intel reported Q1 2026 on April 23, 2026, marking the sixth consecutive quarter of beats. Revenue $13.6B (+7.2% YoY) cleared the high end of guidance ($12.7B) by over $900M; non-GAAP EPS $0.29 was 29x the $0.01 consensus. But more important than the headline numbers is the structural change in segment-level profitability.

DCAI revenue $5.1B (+22% YoY), up from $4.1B. Operating margin expanded 16.6pp from 13.9% to 30.5%, OP $1.5B. This is unmistakable evidence of structural transition in a single quarter.

The multi-year Xeon + custom IPU agreement with Google — 'AI training and inference workloads running on Google Cloud' — should be read as adoption of a heterogeneous AI system reference platform, not a one-time chip sale. Intel also secured Terafab foundry contracts with SpaceX, xAI, and Tesla (the Elon Musk partnership).

Foundry revenue $5.4B (+20% QoQ); external foundry revenue is small at $174M but the direction is set. 18A is rated 'better-than-expected' on yield; 14A is reported as more mature than 18A at the same stage. TrendForce, however, warns that 18A yield risk could push Xeon 6+/7 into 2027.

CFO David Zinsner: Advanced Packaging upgraded from 'hundreds of millions per customer' to 'tens of billions annually.' Malaysia back-end expansion to convert into revenue in 2027. Intel will repurchase the 49% stake in the fab business sold to Apollo in 2024 for $14.2B — a deliberate signal of foundry control (a 27% premium over the $11.2B sale price).

Q2 2026 mid-point guidance of $14.3B implies +10% YoY and +5% QoQ, beating $13.0B consensus by $1.3B (+10%). Non-GAAP gross margin guidance of 39.0% expands +9.3pp YoY. The CFO described H2 2026 as 'server up, PC down' per typical seasonality — a strong signal of persistent server CPU demand.

> CEO Lip-Bu Tan, Earnings Call (Verbatim) > 'The mix of server CPUs that customers deploy alongside accelerators is moving toward CPU. The CPU is being repositioned as the indispensable foundation of the AI era. This is not our wishful thinking — it is what we hear from customers.'

The single most important earnings call statement was the CFO's admission that Intel is 'absolutely constrained.' Q1 was the trough, with improvement expected from Q2, but 'we would have had higher revenue if we had more supply.' Management acknowledged it is deliberately reallocating low-end client PC capacity to data center products — a strong signal of demand exceeding supply.

In an unusually direct disclosure, the CFO further warned in guidance that 'memory, wafer, and substrate supply constraints and price increases could affect demand for our products at some point this year.' That Intel — the demand side — is naming supply-side pressure means the structural shortage NVIDIA witnessed in 2024~25 has now spread to x86 CPUs.

This is the starting point of the entire report. The shortage is not a 'special event' confined to NVIDIA Hopper/Blackwell, but a structural phenomenon operating simultaneously across Intel, AMD, memory, substrates, and packaging.

Sign in with Google to unlock the full body of every free report instantly.

Sign in with GoogleThis site runs on ads — the tier system rewards community contributions.

This report is provided for informational purposes only and does not constitute a recommendation to buy or sell any financial instrument. Investment decisions should be made based on your own judgment and responsibility. The analysis and opinions contained herein are based on information available at the time of writing and are subject to change.