Who Pays for Memory — Four Payment Channels and a Redrawn Contract Map

The buyer map and the contract map — dissecting the AI memory bill down to channel, company, and contract. The thinnest point on this map is that the largest new buyer, which reserved 40% of the world's DRAM, is a loss-making company

The payer of the memory bill is not 'the market' but an identifiable few of companies and contracts. The money comes from four wallets in different forms — the hyperscalers' profit-and-loss and borrowing, venture and sovereign capital, and the consumer's device price. Those contracts are now written in the supplier's favor as never before, and part of future payment is already deposited in the form of prepayments. The remaining question is not whether demand is real, but whether the thinnest wallet, Stargate, can turn signatures into cash.

Reader's Brief — 30-second TL;DR

Advanced

Why Now

The contract map has been redrawn in a single year. Micron disclosed 16 strategic customer agreements (a ~$100 billion minimum, $22 billion in prepayments); SK hynix runs the only long-term contracts with the price cap removed; and Samsung and SK hynix signed a letter of intent with OpenAI's Stargate for 900,000 wafers a month (about 40% of the world's DRAM). To this is added a scene of payment-chain inversion, in which customers buy lithography tools on the supplier's behalf and fund fab expansion.

Winners ?? Losers

The four wallets' capacity is not uniform. Channel 1 (hyperscaler direct) is thick but its increment leans on debt. Channel 2 (HBM) sits behind the Nvidia gate, but the wallet is ultimately the same as Channel 1. Channel 3 (Stargate) is the thinnest — a loss-making payer and a double link overlap. Channel 4 (devices) does not collapse but adjusts by volume. The priority for monitoring is contract-execution indicators: Micron's prepayment receipts, the Stargate LOI's conversion into binding contracts, hynix's July 29 results, and Samsung's confirmed results at month-end.

Watch For

Reading depth

Part 1 — The Buyer Map: Four Payment Channels

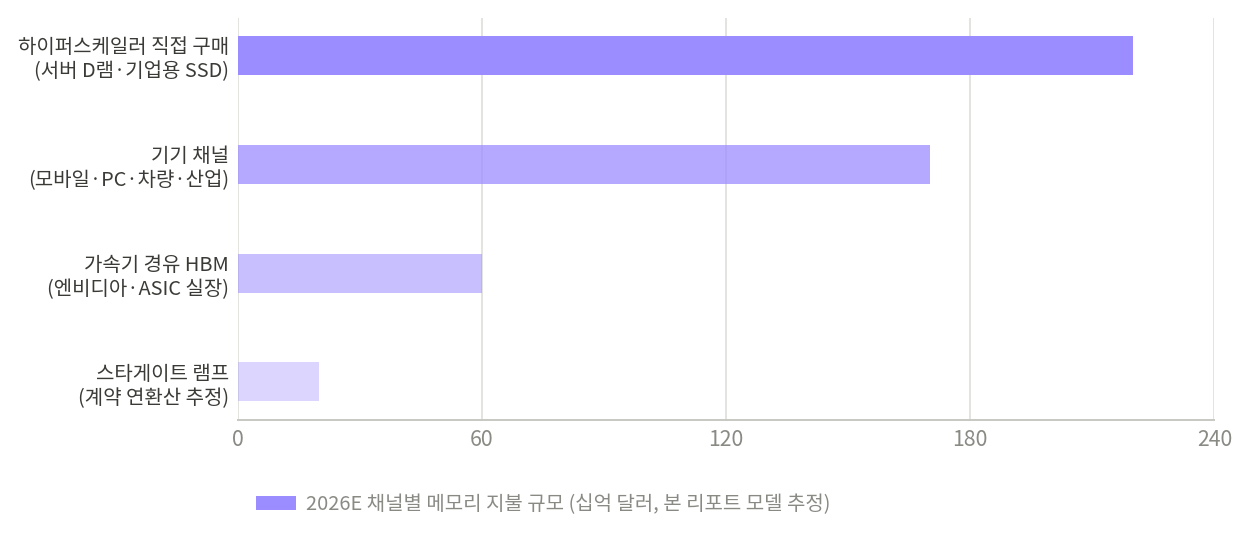

Break down -industry revenue for 2026 by who pays, and four channels emerge. Estimates market size diverge sharply by institution. The early-year forecast from the World Semiconductor Trade Statistics (WSTS) put memory at $294.8 billion. Omdia's April revision, reflecting the price surge, laid out a path in which DRAM doubles year over year and NAND rises up to fourfold. This report's sum of the three suppliers' consensus paths is about $620 billion. The channel breakdown below is based on that upgraded path.

<Chart 1> Memory payment by channel (2026 estimate, $ billions)

Channel 1 — Direct Purchase, $220 Billion a Year

Hyperscalers buy server DRAM and enterprise SSDs directly from suppliers. Memory accounts for 30% of these data-center outlays this year — four times the 2023 level. Applying that share to the four companies' $725 billion in capex puts direct purchases at about $220 billion a year. Microsoft pointed to $25 billion of its $190 billion capex as the memory-and-component price increase.

Company

Capex

Direct memory burden (est.)

Note

Amazon

~$200B

~$60B

Free cash flow seen turning negative

Microsoft

~$190B

~$57B

$25B of the increase is memory pricing

Alphabet

$175–185B

~$54B

—

Meta

$115–135B

~$38B

Weighing sale of compute resources

Total

~$725B

~$220B

30% applied uniformly

Company

Amazon

Capex

~$200B

Direct memory burden (est.)

~$60B

Note

Free cash flow seen turning negative

Company

Microsoft

Capex

~$190B

Direct memory burden (est.)

~$57B

Note

$25B of the increase is memory pricing

Company

Alphabet

Capex

$175–185B

Direct memory burden (est.)

~$54B

Note

—

Company

Meta

Capex

$115–135B

Direct memory burden (est.)

~$38B

Note

Weighing sale of compute resources

Company

Total

Capex

~$725B

Direct memory burden (est.)

~$220B

Note

30% applied uniformly

The mark of this channel is that price tolerance is still high. Samsung Electronics and SK hynix demanded up to 70% server-DRAM increases in January, and subsequent quarterly results show much of it stuck. But the 30% share is itself a brake. Buyer resistance begins at the point where memory starts crowding out the shares of GPUs and power. Meta's review of selling surplus compute was the first signal.

Direct purchase has the deepest capacity to pay. But that capacity has a line drawn by the buyer itself. The moment memory encroaches on the GPU's place, the largest wallet resists first.

Channel 2 — HBM via the Accelerator, With Nvidia as the Gate

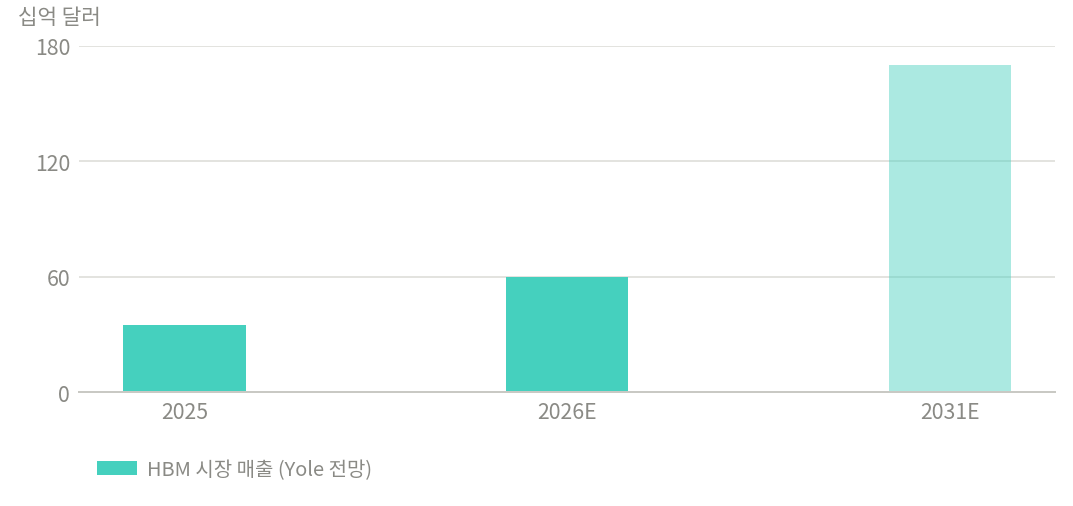

HBM is not bought directly by the end user. It ships mounted on GPUs and accelerators, so the largest buyer is Nvidia. The bill is embedded in the GPU price and is ultimately borne by hyperscalers and . The HBM market grows from about $35 billion in 2025 to about $60 billion in 2026 — up 70% in a single year — with about $170 billion projected for 2031.

Supply allocation is what to watch in this channel. SK hynix signed a multi-year co-development and supply deal with Nvidia and is understood to have secured about two-thirds of the HBM4 volume for the next-generation Rubin platform. Micron began mass-production shipments of Rubin-class HBM4 in May, crossed $1 billion in HBM4 revenue in June, and targets an HBM share in the low-20% range by year-end. A second buyer tier is also growing: as Google and Amazon adopt HBM3E in their own AI chips, cloud operators now account for more than 70% of final HBM demand. Nvidia holds the gate by pre-booking 60–65% of TSMC's advanced-packaging capacity.

HBM sells through the gate that is Nvidia. But the source of the money is, in the end, the cloud operator. There is one gate, and the wallet behind it is the same as Channel 1.

Channel 3 — Stargate, the New Buyer That Reserved 40% of the World's DRAM

OpenAI signed a memory letter of intent with Samsung Electronics and SK hynix for Stargate. The target volume is 900,000 DRAM wafers a month. With global DRAM output capacity at about 2.25 million wafers a month, that is roughly 40% — more than double the world's current HBM capacity. Analysts have valued the order at more than 100 trillion won, about $70 billion, through 2029.

The payment structure of this channel is indirect in three layers. OpenAI commits to $300 billion of compute purchases from Oracle over five years. Oracle and SoftBank build the data centers. Samsung and hynix supply the memory that goes into those servers. The source of Stargate's memory bill is not OpenAI's revenue but Oracle's borrowing and the capital of SoftBank and investors. The double link flagged in the companion piece 'Changing of the Wallet' — a structure in which the money circulates only if both links hold — finds its largest physical instance in this channel.

Stargate is the fastest-growing channel. But the source of its money is not revenue; it is borrowing and capital. The speed of growth and the thinness sit in the same channel.

Channel 4 — Devices, the Last Layer Passed to the Consumer

Mobile, PC, automotive, and industrial make up the traditional channel, about 30% of memory shipment volume. As the AI channels absorb volume, procurement costs in this channel have surged, and pass-through is already under way. Apple raised device prices. Samsung notified Chinese customers of a 20% DRAM increase. PC and smartphone manufacturing costs rose visibly. Automotive has emerged as a new channel: the customer agreement Micron and GM signed on July 1 locked in long-term supply of low-power DRAM, NOR, and UFS NAND for vehicle platforms. For the sake of supply predictability, an era has opened in which automakers sign multi-year deals directly with memory makers.

The final payer of the four channels differs. Channels 1 and 2 are the hyperscalers' profit-and-loss and borrowing. Channel 3 is venture and sovereign capital and the bond market. Channel 4 is the consumer's device price.

The four channels' final payers do not converge into one. They split across the hyperscalers' earnings, the bond market, sovereign capital, and the price on a consumer's device. Where the weight of payment falls differs by channel.

Part 2 — The Contract Map: Who Signed What

Key Points

—The contract map is itself a record — a record that memory has been reclassified from commodity to strategic asset.

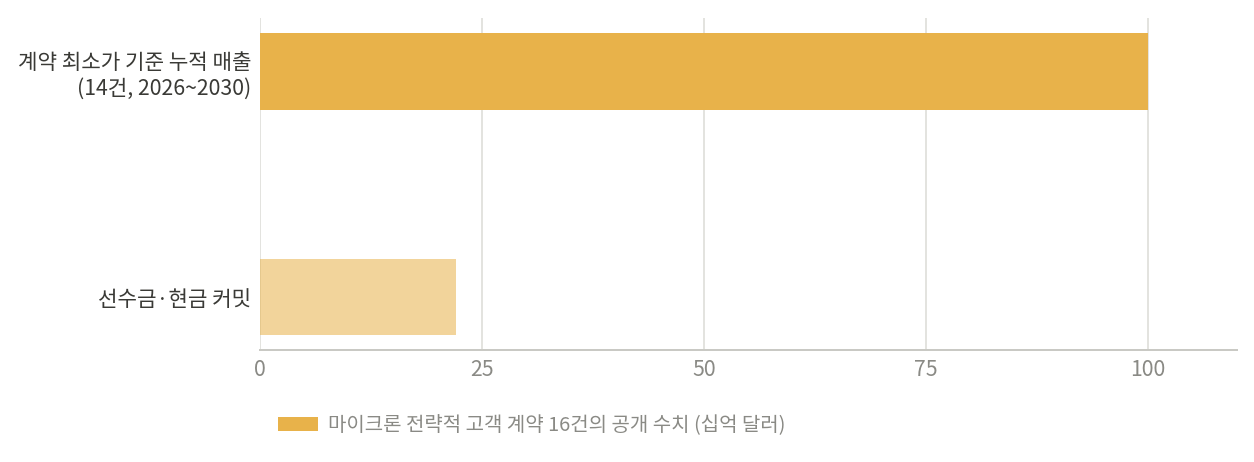

Micron — 16 Deals, $100 Billion, $22 Billion in Prepayments

Micron disclosed 16 strategic customer agreements (SCAs). As of the fiscal third-quarter conference call, the deals with quantified minimum prices carry cumulative revenue of about $100 billion over the remaining terms, with $22 billion in prepayments and other cash commitments due to be received. The terms run five years, from 2026 to 2030, with automotive at three. The counterparties include 'four mega-scale customers and three mid-size customers' — a customer group that had never before agreed to long-term contracts signing for the first time. The only disclosed counterparty is GM; the rest are undisclosed, though the segment mix suggests hyperscalers and large OEMs are the core.

The structure of the pricing clause matters. The price cap for existing products was set at the second-quarter 2026 market price, and volume is a binding clause. Micron's contract is a design that fixes price near current levels and locks in volume. It gives up some upside in exchange for downside defense and prepayments. On a minimum-price basis, a revenue layer of about $20 billion annualized exists through 2030.

Micron gave up the cap and bought the floor. The $100 billion minimum and $22 billion in prepayments are a profit floor that does not vanish even in a downcycle.

SK hynix — The No-Cap Contract and Customer-Funded Capex

SK hynix chose the exact opposite design. It removed from its long-term contracts the price cap that had been the industry standard. Under this structure, if spot prices rise on tight supply, the increase flows straight into the contract price. It is the only large supplier running such contracts. It opened the upside in exchange for giving up some of the stability premium — the mirror image of Micron's trade.

With Nvidia it signed a multi-year memory co-development and supply deal, securing roughly two-thirds of Rubin-generation HBM4 volume. Around this company the most dramatic scene of the payment-chain inversion is unfolding. As capacity ran out, customers stepped up to buy lithography tools on its behalf, and offers even came in to fund new fab lines. A buyer financing the supplier's capex is the extreme of a seller's market, and it is also evidence of both sides' shared view that the shortage runs through 2027. The company plans to double wafer capacity within five years.

hynix removed the cap and opened the upside. A phase in which customers buy the equipment on your behalf is a signal that not the contract but the payment chain itself has inverted.

Samsung Electronics — Contracts in Progress, a 70% Increase Demanded

On its first-quarter call, Samsung Electronics said it is pursuing memory long-term supply agreements at customer request and has already signed with some. At the semiconductor division's global strategy meeting, customer-specific supply strategy for HBM3E and next-generation HBM4/HBM4E was on the table, as was the long-term-contract strategy with large cloud and big-tech customers pursued since early in the year. Pricing power is already being exercised — the demand for up to 70% server-DRAM increases at the start of the year is the proof. The preliminary second-quarter results released on July 7 showed revenue of 171 trillion won and operating profit of 89.4 trillion won — a record that beat the 85-trillion-won consensus, with the margin showing that the increases actually stuck. The disclosure of contract detail — cap or no cap, minimum price, volume — at the confirmed-results call later this month is the biggest thing to watch.

Samsung is still in progress on the contract map. The preliminary results confirmed the price increases stuck. What remains is the disclosure of the contract structure.

Contract Structure Compared — Cap, Floor, Volume, Term

Item

Micron (SCA)

SK hynix (LTA)

Samsung (LTA)

Price cap

Yes — set at 2Q26 market price

No — uniquely removed, reflects spot rise

Undisclosed (in progress)

Minimum-price defense

14 deals, cumulative ~$100B

Undisclosed

Undisclosed

Volume clause

Binding volume commitment

Multi-year supply locked (Nvidia et al.)

Some customers signed (disclosed)

Term

5 yrs (2026–2030), auto 3 yrs

Multi-year (incl. Nvidia co-dev)

Undisclosed

/financing

$22B prepay/commit

Customer tool-buying, fab funding offers

Undisclosed

Disclosed counterparty

GM (15 others undisclosed)

Nvidia, OpenAI (Stargate LOI)

OpenAI (Stargate LOI), some cloud

Design philosophy

Price fix + downside defense + prepay

Upside open — maximize cycle profit

Customer-tailored (incl. HBM4E gen)

Item

Price cap

Micron (SCA)

Yes — set at 2Q26 market price

SK hynix (LTA)

No — uniquely removed, reflects spot rise

Samsung (LTA)

Undisclosed (in progress)

Item

Minimum-price defense

Micron (SCA)

14 deals, cumulative ~$100B

SK hynix (LTA)

Undisclosed

Samsung (LTA)

Undisclosed

Item

Volume clause

Micron (SCA)

Binding volume commitment

SK hynix (LTA)

Multi-year supply locked (Nvidia et al.)

Samsung (LTA)

Some customers signed (disclosed)

Item

Term

Micron (SCA)

5 yrs (2026–2030), auto 3 yrs

SK hynix (LTA)

Multi-year (incl. Nvidia co-dev)

Samsung (LTA)

Undisclosed

Item

Prepayment/financing

Micron (SCA)

$22B prepay/commit

SK hynix (LTA)

Customer tool-buying, fab funding offers

Samsung (LTA)

Undisclosed

Item

Disclosed counterparty

Micron (SCA)

GM (15 others undisclosed)

SK hynix (LTA)

Nvidia, OpenAI (Stargate LOI)

Samsung (LTA)

OpenAI (Stargate LOI), some cloud

Item

Design philosophy

Micron (SCA)

Price fix + downside defense + prepay

SK hynix (LTA)

Upside open — maximize cycle profit

Samsung (LTA)

Customer-tailored (incl. HBM4E gen)

The difference among the three designs is a difference in profit profile by cycle phase. In an upswing, hynix with no cap is favored. In a downturn, Micron with its $100 billion minimum and prepayments is favored. The market remembers past long-term contracts as renegotiated or leaving suppliers holding inventory. These contracts are different. The very direction of renegotiation has flipped to the supplier's advantage — the cap is removed — and clauses absent in the past, prepayments and capex financing, are attached.

A year ago, memory contracts were quarterly price negotiations. Now, five-year volume binding, a $100 billion minimum, $22 billion in prepayments, cap removal, and customer offers to fund fabs all sit in one place.

The contract map is itself a record — a record that memory has been reclassified from commodity to strategic asset.

Full access requires a free account

Sign in with Google to unlock the full body of every free report instantly.

This site runs on ads — the tier system rewards community contributions.

Comments

This report is provided for informational purposes only and does not constitute a recommendation to buy or sell any financial instrument. Investment decisions should be made based on your own judgment and responsibility. The analysis and opinions contained herein are based on information available at the time of writing and are subject to change.